Insurance in home loan is a policy that protects the lender from financial loss in case the borrower defaults on the loan. It provides security to the lender, ensuring that the loan amount will be repaid in case of unforeseen circumstances such as the borrower’s death, disability, or loss of employment.

This type of insurance is mandatory in some countries, while optional in others, and typically the premium is added to the loan amount. It offers peace of mind to both the lender and the borrower, ensuring that the home loan is protected against unexpected events that may impact the borrower’s ability to repay.

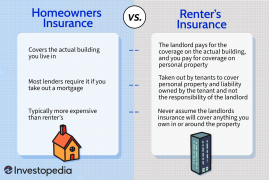

The Basics Of Insurance

Types Of Home Insurance

There are several types of home insurance, including:

- Property Insurance: Covers the structure of the house against damages.

- Liability Insurance: Protects homeowners from liability for injuries or damage to others.

- Personal Property Insurance: Covers personal belongings inside the house.

Importance Of Home Insurance

Having home insurance is crucial because:

- Protection: It safeguards your home against unforeseen events like natural disasters.

- Peace of Mind: You can rest assured that your property is protected.

Home insurance is a smart investment for homeowners to protect their assets.

Understanding Home Loans

Types Of Home Loans

When it comes to purchasing a home, many people require the assistance of a home loan to make their dream a reality. There are a few different types of home loans available, each designed to suit different financial situations.

How Home Loans Work

Home loans provide a way for individuals to purchase a home without having to pay the full purchase price upfront. In exchange for a loan from a bank or lending institution, the borrower agrees to repay the loan amount, plus interest, over a set period of time.

Insurance Requirements For Home Loans

When it comes to home loans, insurance plays a crucial role in providing financial protection to both borrowers and lenders. Insurance requirements for home loans can vary depending on several factors, including the type of loan, the lender’s policies, and the borrower’s circumstances. In this article, we will explore the insurance requirements for home loans and discuss the difference between mandatory and optional insurance. We will also delve into the factors that influence these requirements. So, let’s get started!

Mandatory Vs. Optional Insurance

Mandatory insurance, as the name suggests, is required by the lender as a condition for approving the home loan. It is designed to protect the lender’s investment in case of unforeseen events such as natural disasters or accidents. Generally, the two main types of mandatory insurance for home loans are hazard insurance and mortgage insurance.

Hazard insurance (also known as homeowner’s insurance) provides coverage for property damages caused by events like fire, theft, or storms. This insurance not only protects the lender’s interest but also safeguards the borrower’s investment in the property. It is usually a requirement for both conventional and government-backed home loans.

Mortgage insurance, on the other hand, is usually required for borrowers who have a down payment of less than 20% of the home’s purchase price. This insurance protects the lender if the borrower defaults on the loan. It allows borrowers who may not meet the traditional down payment requirements to obtain a home loan. Mortgage insurance can be provided by private companies or through government programs like the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA).

Optional insurance, as the name suggests, is not mandatory but recommended for borrowers. It provides additional protection and peace of mind for homeowners. Some examples of optional insurance for home loans include flood insurance, earthquake insurance, and identity theft insurance. Although these insurances are not typically required by lenders, they may be necessary depending on the property’s location and individual circumstances.

Factors Influencing Insurance Requirements

Several factors influence the insurance requirements for home loans. These factors can vary depending on the lender and the borrower’s specific circumstances. Some of the key factors include:

- The type of loan: Different types of loans have different insurance requirements. For example, conventional loans often require private mortgage insurance (PMI) if the borrower’s down payment is less than 20%, while government-backed loans like FHA loans require mortgage insurance regardless of the down payment.

- The loan-to-value ratio (LTV): The LTV ratio is calculated by dividing the loan amount by the appraised value of the property. Higher LTV ratios often result in higher insurance requirements.

- The borrower’s credit score: A borrower with a lower credit score may face higher insurance requirements, as they may be considered higher risk by lenders.

- The location of the property: Properties located in high-risk areas, such as flood zones or earthquake-prone regions, may require additional insurance coverage.

- The borrower’s financial situation: Lenders may consider factors like the borrower’s income, employment history, and debt-to-income ratio when determining insurance requirements.

By understanding the difference between mandatory and optional insurance and considering the factors that influence these requirements, borrowers can make informed decisions and ensure they have the right level of protection for their home loans.

Choosing The Right Insurance

When taking out a home loan, having the right insurance in place is crucial to protect your investment. From lenders mortgage insurance to home and contents insurance, there are various policies to choose from. The key is to select the right insurance that offers comprehensive coverage and fits your specific needs.

Comparing Insurance Policies

When choosing the right insurance for your home loan, it’s essential to carefully compare different policies. Comparing the coverage, premiums, and exclusions across various insurance providers will help you make an informed decision. Utilize online resources and seek advice from reputable insurance agents to gain a comprehensive outlook on the available options.

Factors To Consider When Choosing Insurance

Several factors should be taken into account when selecting insurance for your home loan. Consideration of factors such as the level of coverage, premium affordability, claim process efficiency, and reputation of the insurance provider are paramount. Be sure to pay attention to any additional benefits or features offered within the policy that align with your specific requirements.

Insurance Premiums And Costs

When it comes to home loans, understanding insurance premiums and costs is crucial for borrowers. Insurance in home loans provides financial protection against risks like accidents, natural disasters, or death. It ensures that the loan is repaid even if unforeseen situations arise.

Factors Affecting Premiums

- Property Value: The cost of insurance is often based on the value of the property being insured.

- Location: Properties in high-risk areas may have higher premiums due to increased chances of damage.

- Policy Coverage: The extent of coverage and add-ons chosen can impact the insurance premium.

- Security Measures: Homes with security systems or safety features may qualify for lower premiums.

Ways To Lower Insurance Costs

- Compare Quotes: Obtain multiple quotes to find the most competitive insurance premium.

- Improve Home Safety: Install smoke alarms, security systems, or storm shutters to reduce risks.

- Higher Deductibles: Opting for a higher deductible can lower monthly insurance costs.

- Bundling Policies: Combining home and auto insurance with the same provider can lead to discounts.

Claims Process And Coverage

When it comes to securing your home loan, understanding the insurance claims process and coverage is crucial. This knowledge will help you navigate the complexities of insurance and ensure your most significant investment is protected. Let’s delve into the essential aspects of the claims process and coverage when it comes to insurance in a home loan.

How To File A Claim

Filing an insurance claim for your home loan is a systematic process. It involves notifying your insurance company of the incident, providing necessary documentation, such as photos and receipts, and cooperating with the investigation. The filing process can vary depending on the type of claim, but the essential steps remain the same.

Understanding Coverage Limits

One critical aspect of insurance in a home loan is understanding the coverage limits. The coverage limits determine the maximum amount a policy will pay for a covered loss. It’s crucial to review and comprehend the specifics of your coverage limits to ensure you have adequate protection for your property.

Common Insurance Pitfalls

When it comes to securing insurance for your home loan, there are several common pitfalls that many homeowners fall into. It is important to be aware of these pitfalls to ensure that you have adequate coverage in the event of any unforeseen circumstances. In this article, we will discuss two common insurance pitfalls that homeowners should avoid: underinsuring property and not understanding policy exclusions.

Underinsuring Property

One common pitfall that homeowners often encounter is underinsuring their property. Underinsuring your property means that the amount of insurance coverage you have falls short of the actual value of your home. This can happen if the homeowners fail to accurately assess the value of their property or if they choose a lower coverage amount to save on insurance premiums.

Underinsuring your property can have serious consequences. In the event of a total loss, such as a fire or natural disaster, the insurance payout may not be enough to cover the cost of rebuilding or repairing your home. This can leave you with a significant financial burden and potentially leave you homeless.

Therefore, it is crucial to accurately assess the value of your property and choose an insurance coverage amount that adequately reflects its worth. This can be done by working with a qualified appraiser or consulting with insurance professionals who can help determine the appropriate coverage amount based on the specific characteristics of your home.

Not Understanding Policy Exclusions

Another common pitfall in home loan insurance is not fully understanding the policy exclusions. Policy exclusions are specific situations or events that are not covered by your insurance policy. If you are not aware of these exclusions, you may mistakenly assume that you are protected when, in fact, you are not.

Policy exclusions can vary depending on the insurance provider and policy type. Some common exclusions include damages caused by natural disasters like earthquakes or floods, acts of war or terrorism, or maintenance-related issues. It is essential to carefully review your insurance policy and understand the exclusions to avoid any surprises in the event of a claim.

By familiarizing yourself with the exclusions, you can make informed decisions about additional coverage options you may need to consider. This might include purchasing separate policies for specific risks not covered by your primary home insurance policy.

In conclusion, it is crucial to avoid these common insurance pitfalls when securing home loan insurance. By accurately assessing the value of your property and understanding policy exclusions, you can ensure that you have the right coverage and avoid any potential financial hardship in the future.

Staying Informed And Updated

Insurance in home loan is a crucial part of staying informed and updated. It provides protection and coverage for unexpected events that can impact your property, giving you peace of mind and financial security. Secure your investment with the right insurance policy tailored to your needs.

Staying Informed and UpdatedReviewing Policies Annually

Review your home loan insurance policies every year. Understand any changes that may affect coverage.

Check for any modifications in terms and conditions. Ensure your policy aligns with your needs.

Evaluate the adequacy of your coverage annually. Make adjustments as per your current situation.

Seeking Professional Advice

Consult with insurance experts. Gain insights into the best insurance plans for your home loan.

Get professional guidance on policy selections. Ensure you are adequately protected.

Seek advice on any policy changes needed. Stay informed about potential improvements.

Frequently Asked Questions For What Is Insurance In Home Loan

What Is Home Loan Insurance?

Home loan insurance provides financial protection in case of unexpected events such as death or disability, ensuring the loan is repaid. It offers peace of mind to both the borrower and the lender, safeguarding the investment in the property.

Why Do I Need Home Loan Insurance?

Home loan insurance ensures that your family is not burdened with the loan in case of unfortunate events. It provides financial security and helps prevent the risk of foreclosure, allowing your loved ones to stay in their home.

How Does Home Loan Insurance Work?

Home loan insurance works by covering the outstanding loan amount in case of the borrower’s demise, thus preventing the financial burden from falling on the co-borrower or family members. It provides a safety net for the family and protects their home.

Conclusion

To sum up, insurance is a crucial component of a home loan. It provides protection to both lenders and borrowers in case of unforeseen circumstances such as natural disasters, accidents, or loss of income. By having adequate insurance coverage, homeowners can ensure that their investment is safeguarded and their financial well-being is protected.

It is important to carefully evaluate and choose the right insurance policy that suits your specific needs and circumstances. Remember, being proactive and prepared is always better than facing financial uncertainties in the future.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “What is home loan insurance?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Home loan insurance provides financial protection in case of unexpected events such as death or disability, ensuring the loan is repaid. It offers peace of mind to both the borrower and the lender, safeguarding the investment in the property.” } } , { “@type”: “Question”, “name”: “Why do I need home loan insurance?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Home loan insurance ensures that your family is not burdened with the loan in case of unfortunate events. It provides financial security and helps prevent the risk of foreclosure, allowing your loved ones to stay in their home.” } } , { “@type”: “Question”, “name”: “How does home loan insurance work?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Home loan insurance works by covering the outstanding loan amount in case of the borrower’s demise, thus preventing the financial burden from falling on the co-borrower or family members. It provides a safety net for the family and protects their home.” } } ] }

Leave a comment