Disability insurance judgment is a legal decision that determines an individual’s eligibility for disability benefits based on their medical condition and ability to work. We will explore the process of disability insurance judgment, the factors considered, and how it affects an individual’s ability to receive financial support in times of disability or illness.

Understanding this process is crucial for those seeking disability benefits, as it can greatly impact their financial stability and overall well-being. So, let’s delve deeper into the world of disability insurance judgment and its significance.

Credit: myfamilylifeinsurance.com

The Importance Of Disability Insurance

Disability insurance is crucial for financial protection in case of a sudden disability. Having this coverage safeguards your income and provides peace of mind. Make informed decisions to secure your future with disability insurance judgment.

Financial Protection

Disability insurance provides financial security if individuals are unable to work due to injury or illness.

- Covers a portion of lost income during disability.

- Helps pay bills and daily expenses when unable to work.

Peace Of Mind

Having disability insurance offers peace of mind knowing that you have a safety net in case of unforeseen circumstances.

- Reduces stress related to financial instability.

- Allows individuals to focus on recovery without worrying about income loss.

Understanding Disability Insurance

Disability insurance is an important and often overlooked form of insurance. It provides financial protection in the event that you are unable to work due to a disability. In this post, we will delve into the key aspects of disability insurance, including its definition, coverage, and the various types available.

Definition And Coverage

Disability insurance, also known as disability income insurance, is a type of insurance that provides income replacement when you are unable to work due to a disability. It is designed to protect individuals and their families from financial hardship in case of an unexpected event that leaves them unable to earn income.

Disability insurance typically covers a portion of your pre-disability income, allowing you to meet your financial obligations and maintain your standard of living. The coverage amount can vary depending on the policy, but it is usually a percentage of your regular income.

| Key Points |

|---|

| Disability insurance provides income replacement when you are unable to work due to a disability. |

| It protects individuals and their families from financial hardship. |

| The coverage amount is typically a percentage of your pre-disability income. |

| Disability insurance ensures that you can meet your financial obligations and maintain your standard of living. |

Types Of Disability Insurance

There are two main types of disability insurance: short-term disability insurance and long-term disability insurance. Let’s take a closer look at each type:

1. Short-Term Disability Insurance

Short-term disability insurance provides coverage for a limited period of time, usually up to six months. It kicks in shortly after you become disabled and typically pays a higher percentage of your income, often up to 80%. This type of insurance is ideal for covering temporary disabilities, such as injuries or illnesses that require a short recovery time.

2. Long-Term Disability Insurance

Long-term disability insurance comes into play when a disability extends beyond the coverage period of short-term disability insurance. It provides coverage for an extended period of time, ranging from several years up to retirement age, depending on the policy. The benefit amount is usually lower than that of short-term disability insurance, but it provides coverage over a longer duration.

- Short-term disability insurance covers temporary disabilities for up to six months.

- Long-term disability insurance provides coverage for an extended period of time, ranging from several years to retirement age.

- Both types of disability insurance are crucial for protecting your income and financial stability.

Understanding disability insurance is essential for safeguarding your financial well-being in the face of unexpected disability. By familiarizing yourself with the definition, coverage, and types of disability insurance available, you can make informed decisions and ensure that you are adequately protected.

Factors To Consider Before Choosing Disability Insurance

Before choosing disability insurance, it is crucial to consider factors such as coverage options, waiting periods, benefit amounts, and policy exclusions. Making an informed judgment will ensure that you select the right plan to protect you financially in case of disability.

Factors to Consider Before Choosing Disability Insurance Income Level When considering disability insurance, your income level should be a primary factor in determining the coverage you need. Those with higher incomes may require more comprehensive coverage to ensure their lifestyle can be maintained in the event of a disability. Alternatively, individuals with lower incomes may opt for more affordable coverage that still adequately protects their financial well-being. Occupation and Job Stability Your occupation and job stability are crucial aspects to consider when selecting disability insurance. High-risk occupations, such as construction or manufacturing, may necessitate more robust coverage due to the increased likelihood of workplace-related disabilities. Moreover, individuals with less stable employment should ensure their coverage offers protection in the event of sudden job loss or instability. Health Status Another critical factor in choosing disability insurance is your health status. Individuals with pre-existing medical conditions or those in poor health may require more comprehensive coverage to account for the heightened risk of disability. Conversely, healthier individuals may opt for more basic coverage, thereby reducing their premium costs. Additionally, age and lifestyle choices should also be considered. Younger individuals may opt for shorter benefit periods, as they have more working years ahead of them, while older individuals may choose longer benefit periods to account for potential long-term disabilities as they near retirement age. In conclusion, carefully assessing your income level, occupation and job stability, and health status is crucial when selecting disability insurance. By considering these factors, you can ensure that your coverage adequately safeguards your financial well-being and provides peace of mind in the event of a disability. I hope this information is helpful for you. Let me know if you need further assistance!Key Features To Look For In Disability Insurance Policies

When it comes to choosing a disability insurance policy, there are several key features to look for in order to ensure you have the appropriate coverage to protect yourself in the event of a disability. Understanding the specific details of a disability insurance policy can be crucial to ensuring you have adequate protection. Here are the key features to look for in disability insurance policies.

Benefit Period

The benefit period refers to the length of time the disability insurance will pay benefits if you are unable to work due to a disability. It is essential to choose a policy with a benefit period that aligns with your specific needs, whether short-term or long-term disability coverage.

Elimination Period

The elimination period, sometimes referred to as the waiting period, is the amount of time that must pass after the onset of a disability before the insurance benefits begin. It is important to consider this period when choosing a policy, as a longer elimination period may result in lower premiums.

Definition Of Disability

The definition of disability outlined in the policy is critical, as it determines the circumstances under which you will be eligible to receive benefits. Look for policies with a liberal definition of disability, such as being unable to perform your specific occupation, to ensure comprehensive coverage.

Common Mistakes To Avoid When Selecting Disability Insurance

Choosing the right disability insurance can be a complex process that requires careful consideration. It’s important to avoid common mistakes that can leave you underinsured or exposed to unnecessary risks. In this article, we will discuss some of the most common mistakes to avoid when selecting disability insurance.

Underestimating Coverage Needs

One of the biggest mistakes individuals make when selecting disability insurance is underestimating their coverage needs. It’s essential to accurately assess the amount of coverage you would require to maintain your lifestyle and meet financial obligations in the event of a disability.

Consider factors such as your current income, monthly expenses, and any outstanding debts or financial commitments. Remember that your disability insurance should aim to replace a significant portion of your income if you become unable to work due to a disability.

To avoid underestimating your coverage needs, it is advisable to consult with a qualified professional who can guide you through the process and help you determine an appropriate coverage amount. They can assess your unique circumstances and consider potential scenarios that you may not have accounted for.

Ignoring Policy Details

Another common mistake is ignoring the policy details when selecting disability insurance. It’s crucial to thoroughly review and understand the terms, conditions, and exclusions of any insurance policy before making a decision.

Many individuals make the mistake of focusing only on the premium amount and not paying enough attention to other crucial aspects such as waiting periods, benefit periods, and elimination periods. These factors can significantly impact your coverage and the time it takes for the policy to kick in.

Additionally, it’s important to carefully consider the definitions of disability outlined in the policy. Some policies may have stricter definitions that make it more challenging to qualify for benefits. Understanding these details can help you make an informed choice and select a policy that aligns with your needs and expectations.

To avoid ignoring policy details, take the time to read through the entire policy document and seek clarification on any aspects that are unclear. Remember that you have the right to ask questions and request additional information from insurance providers before making a decision.

By avoiding these common mistakes, you can ensure that you select the right disability insurance that provides adequate coverage and safeguards your financial well-being in the face of potential disabilities.

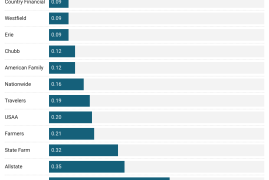

Comparing Disability Insurance Quotes

When it comes to protecting your financial future, disability insurance plays a crucial role. However, choosing the right policy can be overwhelming with multiple options available. That’s why comparing disability insurance quotes is a smart move that can help you find the best coverage at the most affordable rate. In this section, we will explore the importance of getting multiple quotes and reading between the lines of these quotes to make an informed decision. Ready? Let’s dive in!

Getting Multiple Quotes

Getting multiple disability insurance quotes ensures that you have a comprehensive view of the available options. By reaching out to various insurance providers, you gain insight into their different policies, premiums, and benefits. This allows you to compare and contrast the features of each quote side by side, helping you make an informed choice. Moreover, by obtaining multiple quotes, you can negotiate with insurers for better rates and improved terms that suit your individual needs.

Reading Between The Lines

When comparing disability insurance quotes, it’s essential to read between the lines and understand the details provided. Insurance quotes often have fine print that can impact the coverage and terms. By carefully examining the fine print, you can identify any limitations, exclusions, or additional requirements that may affect your policy. Additionally, pay attention to the waiting periods, elimination periods, and definitions of disability. These details can help you determine how quickly and under what circumstances you would receive benefits if you were to become disabled.

Reading between the lines also means considering the financial stability and reputation of the insurance company offering the quote. Look for customer reviews, ratings, and industry rankings to assess their reliability and claims payment history. Remember, the right disability insurance policy not only provides financial protection but also offers peace of mind when you need it the most.

Consulting With A Financial Advisor

When facing the decision of disability insurance, consulting with a financial advisor can provide valuable guidance for protecting your financial future. With the expertise and customized recommendations offered by a financial advisor, you can make informed decisions tailored to your specific needs.

Expert Advice

Financial advisors offer expert advice on disability insurance options that align with your financial goals. They can analyze your current financial situation and provide insight into the type and amount of coverage that would best suit your needs. Their expertise allows for a comprehensive understanding of the intricate details of disability insurance, ensuring that you are well-informed throughout the decision-making process.

Customized Recommendations

Through personalized consultations, financial advisors can craft customized recommendations for disability insurance that cater to your unique circumstances. By considering your income, expenses, and long-term financial aspirations, they can tailor a plan that offers the most suitable coverage to safeguard your financial stability in the event of disability. Such personalized recommendations ensure that your disability insurance aligns with your specific financial situation and goals.

Credit: http://www.amazon.com

Ongoing Review And Adjustments

Regularly reviewing and adjusting your disability insurance policy is crucial to ensure it continues to meet your needs and circumstances. By staying proactive in monitoring your coverage, you can make timely modifications to adapt to life changes and enhance your protection.

Life Changes

Life changes such as marriage, having children, getting a promotion, or starting a new business can impact your financial responsibilities and income. It’s important to review your disability insurance coverage after significant life events to ensure it aligns with your current situation.

Policy Upgrades

As your income grows or your financial obligations increase, you may need to upgrade your disability insurance policy to adequately protect your earnings and assets. Consulting with your insurance provider regularly can help you determine if policy upgrades are necessary.

Credit: bryantlg.com

Frequently Asked Questions On How Disability Insurance Judgement

What Is Disability Insurance?

Disability insurance provides financial protection if you’re unable to work due to illness or injury. It ensures you receive a portion of your income during your absence, offering peace of mind and financial security for you and your family.

How Does Disability Insurance Work?

Disability insurance pays out a percentage of your income if you become disabled and are unable to work. It provides a source of income to cover living expenses and other financial obligations, offering a safety net during challenging times.

Who Needs Disability Insurance?

Anyone who relies on their income to support themselves or their family should consider disability insurance. It provides financial protection in case of unexpected illness or injury, ensuring you can maintain your standard of living even if you can’t work.

What Does Disability Insurance Cover?

Disability insurance typically covers a portion of your income if you’re unable to work due to a qualifying disability. It helps replace lost wages and can be used to cover living expenses, medical bills, and other financial obligations during your recovery.

Conclusion

Disability insurance is a crucial financial safety net that offers support and protection to individuals who are unable to work due to disability or illness. By understanding the judgment process and the importance of thorough documentation, claimants can increase their chances of a successful claim.

It is vital to consult with experienced professionals, thoroughly review policy details, and seek legal advice if necessary. Taking these steps can ensure a smoother process and provide the financial stability needed during difficult times. Remember, disability insurance can be a lifeline when unforeseen circumstances arise.

Leave a comment