On average, a household files around two home insurance claims per year. Home insurance claims vary.

Home insurance claims are a common occurrence that homeowners experience periodically. Having home insurance helps protect against unexpected incidents such as natural disasters, theft, or accidents. By understanding the frequency of home insurance claims, homeowners can make informed decisions about their coverage needs.

Being aware of the typical number of claims can guide individuals in selecting the right insurance policy to safeguard their home and belongings. In the event of a covered loss, having adequate coverage can provide peace of mind and financial protection. It is essential for homeowners to stay informed about home insurance claim trends to ensure they are adequately prepared for any unforeseen circumstances.

The Importance Of Home Insurance

Home insurance is a crucial component of safeguarding your home and protecting your financial investment. It provides peace of mind and financial security in the event of unexpected disasters or property damage. In this post, we explore the importance of home insurance, the benefits it offers, and how it helps you protect your biggest investment.

Protecting Your Biggest Investment

Your home is likely your most significant investment, and it’s essential to safeguard it against potential risks. Home insurance provides protection against a range of perils, including fire, theft, vandalism, and natural disasters, ensuring that you can recover financially from unforeseen events that could damage or destroy your property.

Understanding The Benefits Of Home Insurance

Home insurance offers a host of benefits that go beyond mere property protection. It can cover additional living expenses if you’re forced to leave your home due to a covered loss, provide liability protection in case someone is injured on your property, and offer peace of mind knowing that you have financial protection in place.

Frequency Of Home Insurance Claims

Exploring the Annual Rate of Home Insurance Claims

Home insurance claims occur at various rates throughout the year, impacting homeowners’ financial stability. Understanding the frequency of these claims unveils insights into common scenarios and helps in the protection of one’s assets.

Factors Influencing Claim Frequency

Various factors influence the rate at which home insurance claims are made annually. These factors include:

- Location of the property

- Natural disasters in the region

- Property age and condition

- Presence of security systems

Exploring these factors in detail can provide homeowners with a better understanding of their insurance needs and potential risks they may face.

Types Of Home Insurance Claims

When it comes to home insurance claims, understanding the different types can help you be better prepared for the unexpected. Analyzing common types of claims as well as rare but significant ones can give you a clearer picture of the potential risks your home may face. In this article, we will examine these types in detail to ensure you have a comprehensive understanding of different home insurance claims.

Examining Common Types Of Claims

Common types of home insurance claims encompass incidents that many homeowners encounter at some point. Whether it’s due to natural disasters, theft, or accidents, staying informed about these potential occurrences can help you plan accordingly:

- Weather-related damage: This type of claim often includes damages caused by extreme weather conditions such as storms, hurricanes, or heavy snowfall. It covers repairs or replacements needed due to wind, hail, or water damage.

- Fire and smoke damage: Accidents happen, and if your home suffers from fire or smoke damage, your insurance will likely cover the cost of repairs or rebuilding. It’s crucial to document the damage promptly to ensure a smooth claims process.

- Theft and burglary: Home insurance can protect you financially if you experience theft or burglary. This coverage typically includes stolen personal belongings, damaged property, and any necessary repairs.

- Water damage: Burst pipes, leaking roofs, or faulty plumbing can lead to water damage, which is another common reason for home insurance claims. This coverage is essential, as water damage can result in expensive repairs and potential mold growth.

- Liability claims: Accidents involving guests on your property may result in liability claims. Home insurance can cover medical expenses, legal fees, and potential settlement costs if someone is injured while visiting your home.

Rare But Significant Home Insurance Claims

While less frequent, rare but significant home insurance claims are worth considering due to their potentially devastating consequences. These include:

- Earthquake damage: For homeowners in areas prone to earthquakes, added coverage may be necessary as earthquake damage is typically not covered by standard home insurance policies. This type of claim can involve repair costs for structural and foundation damages caused by seismic activities.

- Flood damage: Similar to earthquake damage, standard home insurance policies generally do not cover flood damage. Homeowners in flood-prone areas should consider obtaining separate flood insurance to protect against this significant risk.

- Mold and fungus: Mold and fungus can be expensive and challenging to eradicate. While some home insurance policies may provide limited coverage for mold, it’s important to understand the specific terms and conditions to ensure adequate protection.

By familiarizing yourself with these rare but significant claims, you can make informed decisions when choosing your home insurance policy and additional coverage options.

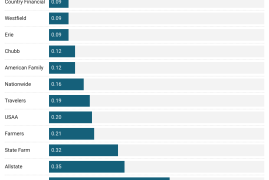

Regional Variances In Claim Frequency

Explore the fluctuations in home insurance claim rates across regions, showcasing the varying frequencies in claims filed annually. Understanding these regional disparities sheds light on factors influencing claim patterns and helps homeowners make informed decisions. Regional nuances play a crucial role in determining the number of home insurance claims submitted each year.

Comparing Claim Rates Across Different Regions

Home insurance claims vary greatly across different regions, and understanding these regional variations is crucial when assessing your own insurance needs. By comparing claim rates across various areas, you can gain insights into the risks specific to your region and make informed decisions regarding your home insurance coverage. Let’s explore the differences in claim frequency between regions.

Factors Contributing To Regional Differences

Several factors contribute to the regional differences in claim frequency. Each region has its own unique set of circumstances that may increase the likelihood of home insurance claims. These factors can include:

- Geographical Location: Geographical location plays a significant role in the frequency and severity of home insurance claims. Areas prone to natural disasters such as hurricanes, earthquakes, or wildfires are more likely to experience higher claim rates.

- Climate and Weather Patterns: The climate and weather patterns of a region greatly influence the risk of home damage. Regions with extreme weather conditions such as heavy rainfall, snowstorms, or high winds are more susceptible to claims related to water damage, roof collapse, and fallen trees.

- Crime Rates: Crime rates in a region can impact home insurance claims. Higher crime rates, including burglary and vandalism, increase the likelihood of claims for stolen or damaged property.

- Housing Density: The density of housing in a region also affects claim rates. Highly populated areas may have a higher risk of accidents, fires, or other incidents that can result in home insurance claims.

- Building Materials and Construction Standards: The materials used in construction and the enforcement of building codes can impact the frequency and severity of home insurance claims. Areas with older buildings or less stringent construction regulations may experience higher claim rates.

By considering these regional differences, insurance providers can better assess the risks associated with specific areas and adjust premiums accordingly. Likewise, homeowners can use this information to determine their insurance needs and take appropriate measures to protect their homes.

Trends In Home Insurance Claims

Trends in Home Insurance Claims:

Emerging Patterns In Claim Frequency

Home insurance claims show noticeable variations year by year.

Increased frequency in weather-related claims observed recently.

Water damage claims on the rise due to aging plumbing systems.

Claims related to theft and vandalism have decreased in certain regions.

Impact Of External Factors On Claim Trends

Factors like climate change influencing patterns in claim frequency.

Economic fluctuations can affect the likelihood of certain claims being made.

Technological advancements leading to changes in security-related claims.

“` In recent years, trends in home insurance claims have been a topic of increasing interest. Emerging Patterns in claim frequency have revealed fluctuations across different categories. For instance, water damage claims have been on the rise due to aging plumbing systems. Contrarily, theft and vandalism claims have shown a decrease in some regions. External factors play a crucial role in Impact of Claim Trends. Climate change, economic shifts, and technological advancements can all influence the frequency and nature of insurance claims. Observing these trends allows insurance providers to tailor their offerings to meet the evolving needs of homeowners.Tips For Managing Home Insurance Claims

When it comes to managing home insurance claims, it’s essential to strategize and take proactive measures. By focusing on maximizing your policy coverage and mitigating risks to reduce claims, you can effectively navigate the process and ensure optimal protection for your home.

Maximizing Your Policy Coverage

Maximizing your policy coverage can significantly reduce the out-of-pocket expenses associated with home insurance claims. Make sure to review and understand the details of your policy to take advantage of all available coverage options. Consider these tips:

- Regularly review and update your policy to ensure it aligns with your current needs and the value of your home.

- Explore additional coverage options such as flood insurance or extended liability coverage to enhance your protection.

- Document your home’s contents and their value to accurately assess your coverage needs and ensure adequate compensation in the event of a claim.

Mitigating Risks To Reduce Claims

Mitigating risks plays a crucial role in minimizing home insurance claims. By implementing precautionary measures, you can reduce the likelihood of damage and the need for claims. Here are some effective strategies:

- Regularly maintain and inspect your home’s structural components to address potential issues before they escalate.

- Invest in preventive measures such as security systems, fire alarms, and disaster-resistant building materials to reduce the risk of property damage.

- Stay proactive with routine maintenance tasks like cleaning gutters, trimming trees, and addressing plumbing leaks to prevent issues that could lead to claims.

The Process Of Filing Home Insurance Claims

The process of filing home insurance claims can be daunting, but understanding the steps involved and potential challenges can help simplify the process. It’s essential for homeowners to be aware of the claim submission process and how to navigate any obstacles that may arise.

Understanding The Claim Submission Process

When a homeowner experiences damage or loss that is covered by their insurance policy, they need to initiate the home insurance claim process. The following steps outline the general procedure for filing a claim:

- Assess the damage: After an incident occurs, assess the damage to your property. Take photos and gather any relevant documentation to support your claim.

- Notify your insurer: Contact your insurance company as soon as possible to report the damage and start the claims process. Be prepared to provide details about the incident and the extent of the damage.

- Meet with an adjuster: Your insurance company may send an adjuster to assess the damage in person. Cooperate fully with the adjuster and provide any additional information they request.

- Receive a settlement: If your claim is approved, your insurer will provide a settlement based on the terms of your policy. Ensure that the amount offered adequately covers the damage and losses sustained.

Navigating Potential Challenges In Claim Filing

While the claim submission process may seem straightforward, homeowners can encounter various challenges when filing a home insurance claim. Some potential obstacles to be aware of include:

- Policy coverage limitations: Familiarize yourself with the exact coverage limits and exclusions in your policy to avoid any surprises when filing a claim.

- Documenting the damage: Accurately documenting the extent of the damage is crucial. Having detailed evidence, such as photos and receipts, can help support your claim.

- Communicating effectively: Clear and prompt communication with your insurer and adjuster is essential to ensure a smooth claims process.

- Resolving disputes: In the event of a dispute over the settlement amount or coverage, be prepared to negotiate with your insurer to reach a satisfactory resolution.

Future Outlook For Home Insurance Claims

On average, the number of home insurance claims per year is increasing due to natural disasters, theft, and accidents. With the evolving landscape of home insurance, policyholders can expect easier claim processes and improved coverage options to better safeguard their homes and possessions.

As homeowners, we must always be prepared for the unexpected. While it is impossible to predict the exact number of home insurance claims we might have in a year, understanding the patterns and trends can help us anticipate potential changes in the future. In this blog post, we will dive into the future outlook for home insurance claims, focusing on two key areas: anticipating changes in claim patterns and innovations in home insurance claim management.

Anticipating Changes In Claim Patterns

Rising extreme weather events: With climate change becoming increasingly evident, the frequency and intensity of extreme weather events are expected to rise. This will likely lead to an increase in home insurance claims related to storms, floods, wildfires, and other natural disasters.

Advancements in technology: The rapid advancements in technology have undoubtedly impacted the modern home. As smart homes continue to gain popularity, the reliance on interconnected devices introduces new risks. Claims arising from hacking, privacy breaches, and tech malfunctions may become more prevalent in the coming years.

Changes in property values: Real estate markets are subject to fluctuations, and changes in property values can influence home insurance claims. As property values rise, the cost to rebuild or repair homes also increases. This can lead to higher claim amounts and potentially impact insurance premiums.

Innovations In Home Insurance Claim Management

Streamlined digital claims process: Insurance companies are investing in user-friendly digital platforms to facilitate a smoother and faster claims process. From filing a claim online to virtual inspections and electronic documentation, these innovations aim to improve efficiency and provide a better customer experience.

Artificial intelligence and data analytics: The integration of artificial intelligence and data analytics has the potential to greatly enhance claim management. By analyzing vast amounts of data, insurance companies can more accurately assess risks, detect fraud, and expedite claim settlement.

Telematics and IoT: The use of telematics and Internet of Things (IoT) devices can greatly aid in preventing and managing home insurance claims. Smart home systems, sensors, and connected devices can detect household issues such as water leaks or security breaches, allowing early intervention and reducing the likelihood of major claims.

By anticipating the changes in claim patterns and staying up-to-date with innovations in home insurance claim management, homeowners can ensure they are adequately protected and prepared for any future claims. Stay informed, be proactive, and choose an insurance provider that embraces the latest advancements in the industry.

Frequently Asked Questions Of How Many Home Insurance Claims Per Year

How Many Claims Is Too Many For Homeowners Insurance?

Having too many claims varies by insurance company, but generally 2-3 within a few years is a red flag. Multiple claims can lead to increased premiums or even policy cancellation. Be mindful of filing unnecessary claims to avoid potential issues.

Which State Has The Most Home Insurance Claims?

Florida has the most home insurance claims in the United States.

What Are The Most Common Claims For Home Insurance?

The most common claims for home insurance include damage from fire, theft, vandalism, water leaks, and acts of nature like storms and earthquakes.

What Percentage Of Homeowners Claims Are Denied?

Approximately 5-10% of homeowners claims are denied by insurers.

Conclusion

Considering the frequency of home insurance claims per year, it is crucial to maintain proper coverage. With the unpredictability of unforeseen events, being prepared can provide peace of mind. Stay informed about your policy and consult with your insurance provider for any clarifications.

Protect your home, protect your future.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “How many claims is too many for homeowners insurance?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Having too many claims varies by insurance company, but generally 2-3 within a few years is a red flag. Multiple claims can lead to increased premiums or even policy cancellation. Be mindful of filing unnecessary claims to avoid potential issues.” } } , { “@type”: “Question”, “name”: “Which state has the most home insurance claims?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Florida has the most home insurance claims in the United States.” } } , { “@type”: “Question”, “name”: “What are the most common claims for home insurance?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “The most common claims for home insurance include damage from fire, theft, vandalism, water leaks, and acts of nature like storms and earthquakes.” } } , { “@type”: “Question”, “name”: “What percentage of homeowners claims are denied?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Approximately 5-10% of homeowners claims are denied by insurers.” } } ] }

Leave a comment