Require enough renters insurance to cover the value of your personal belongings and liability risks. Frequent guidance recommends at least $30,000 to $50,000 in personal property coverage.

Renters insurance is crucial for protecting your belongings and liability in case of unexpected events such as theft, fire, or accidents. Determining the right coverage amount to require involves assessing the value of your possessions and potential risks in your rental property.

By opting for adequate renters insurance coverage, you can secure peace of mind knowing that you are financially protected in challenging situations.

Understanding Renters Insurance

Renters insurance is an essential component of responsible leasing for both landlords and tenants. Understanding the importance of renters insurance is crucial in ensuring that both parties are adequately protected in the event of unforeseen circumstances.

What Is Renters Insurance?

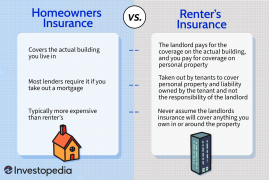

Renters insurance is a policy that provides coverage for a tenant’s personal belongings and liability protection in the rented property. This type of insurance does not cover the building itself as that is the landlord’s responsibility.

Importance Of Renters Insurance

Renters insurance is important as it safeguards tenants against potential financial losses due to theft, fire, vandalism, or other covered perils. It also provides liability coverage in case someone is injured while on the rental premises, protecting the tenant from potential legal action.

Determining Coverage Needs

When it comes to determining coverage needs for renters insurance, two key aspects need consideration; assessing personal property value and considering liability coverage. Let’s break down these factors to help you make an informed decision.

Assessing Personal Property Value

- Determine the value of your belongings, such as furniture, electronics, and clothing.

- Make an inventory to estimate the replacement cost of your possessions.

- Consider special items like jewelry or art that may require additional coverage.

Considering Liability Coverage

- Ensure your policy covers potential damages or injuries that might occur on the rented property.

- Check the coverage limits to confirm they adequately protect your assets.

- Discuss with your insurance provider to understand the extent of liability coverage needed.

Standard Coverage Vs. Additional Options

Standard Coverage vs. Additional Options:

When it comes to protecting your valuable possessions as a renter, having the right insurance coverage is crucial. Renters insurance provides financial protection in the event of theft, damage, or loss, giving you peace of mind during unforeseen circumstances. Understanding the different options available to you is important when determining how much renters insurance to require. In this article, we will explore the difference between standard coverage and additional options for enhanced protection.

Exploring Standard Coverage In Renters Insurance:

Standard coverage in renters insurance typically includes protection for belongings such as furniture, electronics, clothing, and appliances against events like theft, fire, vandalism, and certain natural disasters. It also provides liability coverage, which helps protect you if someone is injured on your property. Additionally, most policies offer coverage for temporary living expenses if your rental becomes uninhabitable due to a covered event.

Additional Options For Enhanced Protection:

While standard coverage may be sufficient for most renters, it’s important to consider additional options for enhanced protection. These options allow you to customize your policy to meet your specific needs and provide extra peace of mind.

- Valuable Items Coverage: If you own expensive items like jewelry, antiques, or collectibles, adding valuable items coverage to your policy ensures these items are adequately protected, even in cases of loss or damage.

- Identity Theft Protection: With the rise of digital dependency, protecting your identity is essential. Opting for identity theft protection can help cover expenses related to identity theft, such as legal fees and lost wages.

- Water Backup Coverage: Standard renters insurance policies usually don’t cover water damage caused by sewer or drain backups. Adding water backup coverage can save you from costly repairs or replacements due to water damage events.

- Personal Injury Liability: While liability coverage is typically included in a standard policy, personal injury liability provides additional coverage for incidents like libel or slander that may occur within your rented space.

- Flood Insurance: Depending on your location, your rental property might be at risk of flooding. Adding flood insurance to your policy ensures you are protected in the event of a flood-related incident.

By exploring these additional options for enhanced protection, you can tailor your renters insurance to better suit your needs and provide greater coverage. Remember, each renter’s situation is unique, so assessing your specific risks and requirements is vital in determining the right amount of coverage to require.

Guidelines For Essential Coverage

If you own rental properties, it is important to establish guidelines to ensure that your tenants have adequate renters insurance coverage. Setting the right coverage limits can help protect your investment, provide peace of mind to your tenants, and minimize your liability. In this blog post, we will discuss the essential coverage guidelines that you should consider when requiring renters insurance. Understanding the minimum coverage requirement, as well as the factors to consider when setting coverage limits, will help you make informed decisions and effectively mitigate potential risks.

Understanding The Minimum Coverage Requirement

Before diving into the factors that influence your coverage limits, it is crucial to understand the minimum coverage requirement. This requirement can vary from state to state and often depends on the value of your rental property. Generally, the minimum coverage includes liability protection, which safeguards both the tenant and the landlord in the event of property damage or bodily injury. It is usually recommended to set a minimum liability coverage of at least $100,000. This coverage helps protect you from costly lawsuits and ensures that your tenants are financially responsible for any damages they might cause.

Factors To Consider When Setting Coverage Limits

Setting the right coverage limits goes beyond the minimum requirement. Several factors can influence the amount of coverage you should require. By carefully considering these factors, you can ensure that your tenants have adequate protection for their personal belongings and any potential risks that may arise within your property. Here are some key factors to consider:

Furniture And Personal Property Value

The value of furniture and personal belongings owned by your tenants should be a primary consideration. Encourage your tenants to conduct a thorough inventory of their possessions and estimate their total value. This can help determine an appropriate coverage limit that will fully protect their belongings in case of theft, fire, or other covered perils.

Location And Risk Factors

The location of your rental property, as well as any inherent risk factors, should be taken into account when setting coverage limits. Properties in areas prone to natural disasters, such as earthquakes or hurricanes, may warrant higher coverage limits. Additionally, if your property has features that increase the risk of accidents, such as a swimming pool or a trampoline, you may want to consider a higher liability coverage limit.

Loss Of Use And Additional Living Expenses

In the unfortunate event that your rental property becomes uninhabitable due to a covered peril, the renters insurance policy should provide coverage for loss of use and additional living expenses. This coverage helps your tenants with temporary accommodation and living costs while repairs are being made. Consider the potential expenses your tenants may incur and ensure the coverage limit is sufficient.

Reviewing Coverage Regularly

Rental property values and risks can change over time. Therefore, it is important to review the coverage requirements periodically. Stay informed about new regulations and insurance market trends so that you can adjust your coverage limits accordingly.

By understanding the minimum coverage requirement and considering the factors mentioned above, you can establish guidelines for essential renters insurance coverage. These guidelines help protect your property, minimize liability risks, and provide your tenants with the peace of mind they deserve. Remember, each property is unique, so it’s important to evaluate the specific circumstances of your rental property and consult with insurance professionals for personalized advice on the optimal coverage limits.

Evaluation Of Deductibles And Premiums

When deciding on renters insurance, evaluating deductibles and premiums is crucial. Here’s how to choose the right deductible and consider premiums for optimal coverage.

Choosing The Right Deductible

- Start by assessing your budget and risk tolerance.

- Higher deductibles usually mean lower premiums.

- Lower deductibles lead to higher premiums but lower out-of-pocket expenses when filing a claim.

Considerations When Evaluating Premiums

- Compare quotes from different insurance companies.

- Check for any available discounts to reduce premiums.

- Review policy coverage limits and exclusions.

Reviewing Policy Exclusions

When reviewing your renters insurance policy, it’s crucial to pay close attention to the exclusions. Understanding what is not covered can help you make informed decisions and avoid potential financial setbacks. Here, we’ll delve into the common exclusions in renters insurance policies and emphasize the importance of grasping these exclusions.

Common Exclusions In Renters Insurance Policies

Natural disasters: Renters insurance typically does not cover damage caused by earthquakes, floods, or hurricanes. While some policies offer optional coverage for these events, they are generally excluded from standard coverage.

- Intentional damage: Any damage caused intentionally by the policyholder is not covered. This includes acts of vandalism or destruction of property.

- Pet-related incidents: Liability for animal bites or property damage by pets may not be included, particularly for breeds perceived as high-risk.

- Business activities: If you conduct business from your rented property, such as running a home-based business, any related liabilities or losses may not be covered.

Importance Of Understanding Policy Exclusions

Preventing surprises: Knowing what your renters insurance does not cover enables you to take additional steps to protect yourself and your belongings from potential risks. By being aware of exclusions, you can explore supplemental policies or alternative solutions to close coverage gaps.

- Avoiding disputes: Understanding exclusions can help mitigate conflicts with insurance companies. By knowing the limitations of your policy, you can avoid filing claims for events that are not covered, leading to a smoother claims process overall.

- Minimizing financial impact: Being informed about exclusions allows you to allocate resources and plan for potential costs that may arise from uncovered events. This proactive approach can help safeguard your financial well-being in the long run.

Comparing Insurance Providers

When it comes to choosing renters insurance, comparing insurance providers is crucial to ensure you get the best coverage at a reasonable price. Researching different insurance companies and weighing their offerings against your needs is essential for making an informed decision. Here are the key factors to consider when comparing insurance providers.

Researching Different Insurance Companies

Before choosing a renters insurance provider, it’s important to conduct thorough research on different insurance companies. Look into the reputation, financial strength, and customer reviews of each company. Additionally, compare the coverage options, deductibles, and premiums offered by different providers to find the most suitable one for your needs.

Factors To Consider When Comparing Insurance Providers

- Coverage Options: Evaluate the types of coverage offered by each insurance company, including personal property, liability, and additional living expenses coverage.

- Deductibles: Compare the deductibles associated with each policy, considering how much you can afford to pay out of pocket in the event of a claim.

- Premiums: Assess the premium costs for various policies and ensure they align with your budget while providing adequate coverage.

- Customer Service: Look for reviews and ratings regarding the customer service and claims process of different insurance companies to gauge their reliability.

- Discounts and Benefits: Inquire about available discounts or additional benefits offered by each provider to maximize the value of your policy.

By carefully considering these factors and comparing insurance providers, you can make an informed decision that safeguards your rental property and belongings without exceeding your budget.

Finalizing Your Renters Insurance Coverage

Ensure sufficient renters insurance for complete protection of personal belongings and liability. Evaluate coverage needs based on asset value, potential risks, and additional endorsements for enhanced security. Consult with insurance providers to determine optimal coverage amounts.

Reviewing The Policy Carefully

Once you have found a renters insurance policy that meets your basic needs, it’s crucial to review it carefully before finalizing your coverage. Taking the time to carefully read through the policy will ensure that you understand what is covered and what is not. Remember, what is included in one policy may differ from another, so it’s essential to compare the details.

Pay close attention to the coverage limits and deductibles. The coverage limit is the maximum amount the insurance company will pay out for a covered claim. You want to make sure that the coverage limits are high enough to fully protect you in case of a significant loss. On the other hand, the deductible is the amount you will have to pay out of pocket before the insurance kicks in. Consider your budget and choose a deductible that you can comfortably afford.

Additionally, read the policy thoroughly for any exclusions or limitations. These are specific situations or damages that the insurance company will not cover. Understanding the exclusions will help you manage your expectations and seek additional coverage if necessary. Keep an eye out for any additional coverages that can be added to your policy, such as coverage for high-value items or liability insurance.

Seeking Professional Advice If Needed

Although renters insurance is relatively straightforward, there may be instances where seeking professional advice can be beneficial. If you are unsure about any aspect of the policy or have specific questions, don’t hesitate to reach out to an insurance agent or broker. They are experts in the field and can provide valuable guidance tailored to your specific needs.

Professional advice can be especially helpful if you have unique circumstances that require additional coverage, such as running a home-based business or owning valuable collections. A knowledgeable professional will be able to assess your situation and recommend appropriate coverage options that meet your specific requirements.

Frequently Asked Questions For How Much Renters Insurance To Require

What Is The Most Common Amount For Renters Insurance?

The most common amount for renters insurance is between $10 to $20 per month.

How Important Is Renters Insurance?

Renters insurance is crucial for protecting your belongings and liability. It provides financial security and peace of mind. If your possessions are damaged or stolen, renters insurance can help cover the costs. In addition, it may offer coverage for temporary living expenses in case of a disaster.

Can A Landlord Require Renters Insurance In Pennsylvania?

Yes, landlords in Pennsylvania can require renters insurance from tenants. It helps protect both parties in case of damages or liabilities.

Can Florida Landlords Require Renters Insurance?

Yes, Florida landlords can require renters insurance as a condition of the lease agreement. It is important to check your lease agreement to see if renters insurance is required.

Conclusion

In determining the right amount of renters insurance, always consider your specific needs and belongings. Be mindful of any potential risks and make an informed decision. Remember, having adequate coverage provides peace of mind and financial security. Select a policy that aligns with your lifestyle and safeguards your possessions.

Leave a comment