General Liability Insurance is not the same as Workers Compensation. General Liability Insurance covers third-party injury or property damage, while Workers Compensation provides coverage for employee work-related injuries and illnesses.

General Liability Insurance protects businesses from lawsuits related to non-employee injuries or property damage, whereas Workers Compensation covers the medical expenses and lost wages of employees injured on the job. As a business owner, it is crucial to understand the distinction between General Liability Insurance and Workers Compensation.

Each insurance type provides specific protections and benefits, ensuring comprehensive coverage for your business. By having the right insurance policies in place, you can safeguard your business, employees, and clients from potential financial losses and legal issues. We will delve deeper into the differences between General Liability Insurance and Workers Compensation, helping you make informed decisions about your insurance needs.

Credit: http://www.embroker.com

Coverage

When it comes to insurance for your business, it’s essential to understand the differences in coverage between General Liability Insurance and Workers Compensation. Let’s delve into the specifics of Coverage:

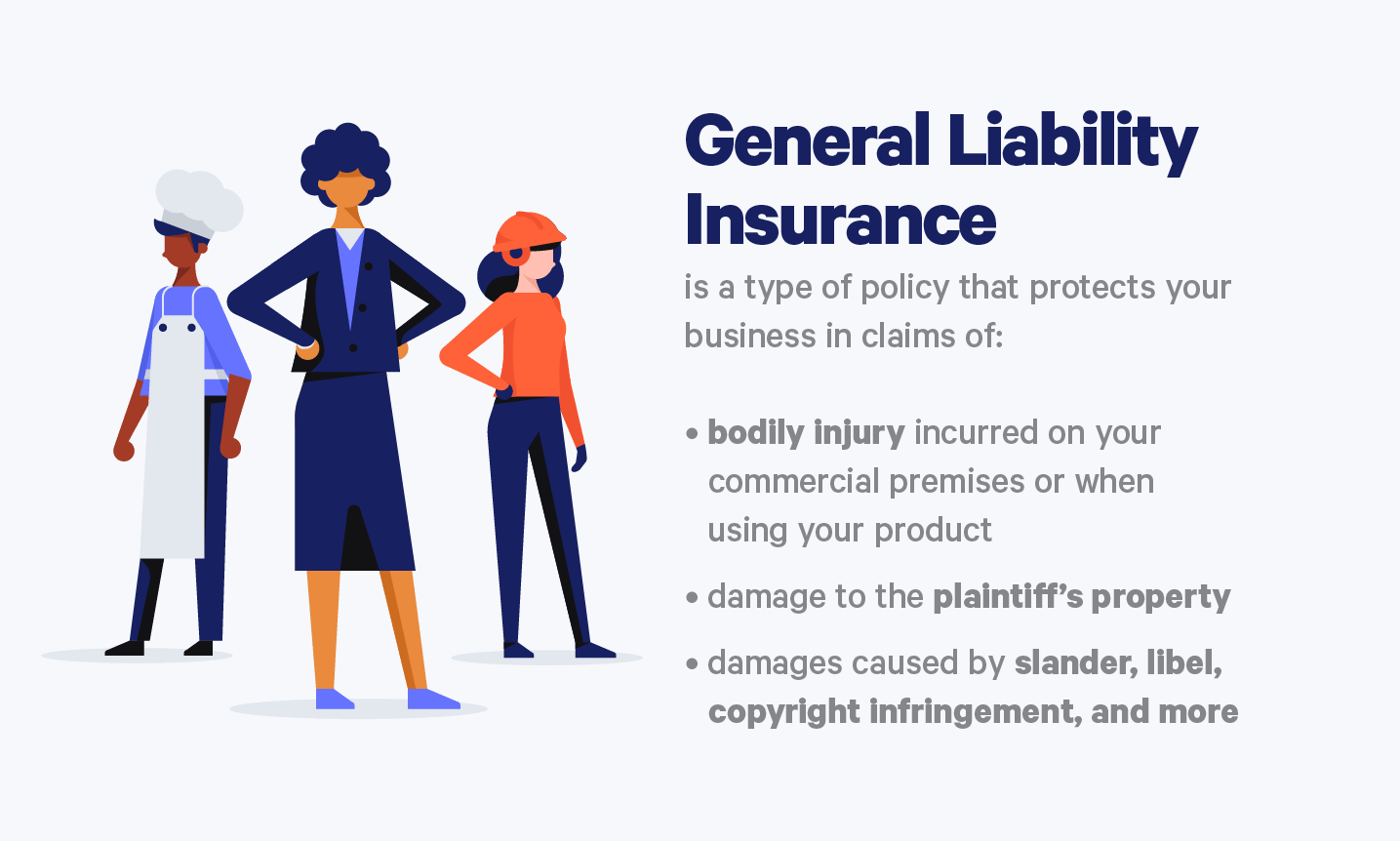

General Liability Insurance Coverage

General Liability Insurance protects your business from claims related to third-party bodily injury or property damage occurring on your business premises.

It covers legal fees and settlements if your business is sued for negligence or accidents causing harm to others.

Workers Compensation Coverage

Workers Compensation provides coverage for employees who suffer work-related injuries or illnesses.

This insurance offers wage replacement and medical benefits to employees injured on the job.

:max_bytes(150000):strip_icc()/Commercial-General-Liability-Final-51e0c0f9b27d4e409a7f49da59fbe037.jpg)

Credit: http://www.investopedia.com

Purpose

When it comes to protecting your business, it’s important to have the right insurance policies in place. Two of the most critical types of insurance coverage for businesses are general liability insurance and workers compensation insurance. These policies serve distinct purposes, and it’s essential to understand how they differ to effectively safeguard your business and employees.

Purpose Of General Liability Insurance

General liability insurance is designed to protect your business from financial losses resulting from third-party claims for bodily injury, property damage, and personal and advertising injury. This type of coverage provides financial assistance in the event that your business is found liable for accidents or negligent actions that cause harm to others.

Here are the key purposes of having general liability insurance:

- Protecting your business assets from lawsuits or claims filed by third parties.

- Covering legal expenses, including attorney fees and court costs, in the event of a lawsuit.

- Providing compensation for bodily injuries sustained by customers, clients, or members of the public while on your premises or as a result of your business operations.

- Offering coverage for property damage caused by your business operations.

- Protecting your business against claims of false advertising, defamation, or copyright infringement.

Purpose Of Workers Compensation

Workers compensation insurance, on the other hand, is specifically designed to provide financial protection to employees who suffer work-related injuries or illnesses. This coverage is mandatory in most states and serves as a safety net for employees, ensuring that they receive compensation for medical expenses, lost wages, and rehabilitation treatments.

Here are the primary purposes of workers compensation insurance:

- Ensuring that injured or ill employees receive prompt medical attention and necessary treatments.

- Providing wage replacement benefits to employees who are unable to work due to their work-related injuries or illnesses.

- Protecting employers from potential lawsuits by injured employees, as workers compensation insurance typically provides immunity against such legal actions.

- Encouraging workplace safety and incentivizing employers to maintain safe working environments to reduce the risk of injuries or illnesses.

- Offering support for rehabilitation services to help employees recover and return to work.

While general liability insurance and workers compensation insurance both serve valuable purposes, they cover different aspects of business risks. General liability insurance focuses on protecting your business from liability claims by third parties, while workers compensation insurance solely addresses the needs of injured or ill employees. It is essential to have both policies in place to comprehensively protect your business and ensure the well-being of your employees.

Claims Process

When it comes to general liability insurance and workers’ compensation, understanding the claims process is essential. This process dictates how a business or individual can access financial assistance in the event of an accident or injury. While both types of insurance serve to protect against potential liabilities, the claims processes differ significantly. By understanding these differences, you can ensure that you are adequately covered and have a clear understanding of what to expect should the need for a claim arise

Claims Process For General Liability Insurance

General liability insurance typically covers claims such as bodily injury, property damage, personal injury, and advertising injury. The claims process for general liability insurance can vary depending on the insurance provider, but it generally follows a similar pattern. Once an incident occurs, the individual or business should notify their insurance provider as soon as possible. The provider will then investigate the claim and determine its validity. If the claim is approved, the insurance company will provide financial compensation to cover the damages. In some cases, the insurer may also provide legal representation if the claim results in a lawsuit.

Claims Process For Workers Compensation

Workers’ compensation insurance is specifically designed to cover work-related injuries and illnesses suffered by employees. The claims process for workers’ compensation typically begins with the injured employee reporting the incident to their employer. The employer then notifies the insurance carrier, and the claim is investigated to determine its validity. If the claim is approved, the injured employee can receive compensation for medical expenses and lost wages. In some cases, workers’ compensation claims may also involve a rehabilitation process to help the employee return to work safely.

Credit: http://www.embroker.com

Required By Law

When it comes to running a business, it’s crucial to understand the legal requirements for insurance coverage. General liability insurance and workers’ compensation are two essential forms of coverage that every business owner should have in place. Let’s take a look at the legal obligations surrounding these two types of insurance.

Legal Requirement For General Liability Insurance

General liability insurance is a fundamental coverage that protects businesses from a variety of risks, including bodily injury, property damage, and advertising injury. While it’s not a statutory requirement in most states, general liability insurance is often considered essential for protecting a business’s financial interests. However, certain industries or business contracts may require it as a condition of doing business. In some cases, potential clients or partners may request proof of general liability coverage before engaging in a business relationship.

Legal Requirement For Workers Compensation

On the other hand, workers’ compensation insurance is a legal requirement in almost every state. This coverage is designed to provide protection for employees who are injured or become ill due to work-related activities. Employers are generally obligated by law to carry workers’ compensation insurance to provide medical benefits and wage replacement for employees who suffer from work-related injuries or illnesses. Failure to carry workers’ compensation insurance can result in severe penalties and legal consequences for the employer.

Cost Factors

General liability insurance and workers’ compensation are not the same. The cost factors for both policies differ based on the coverage, industry, and risk levels. It is important to understand the distinction between the two to ensure adequate protection for your business and employees.

Factors Affecting General Liability Insurance Costs

When it comes to protecting your business, both general liability insurance and workers compensation insurance play crucial roles. However, it’s important to understand that these two types of insurance are not the same. In this blog post, we will focus on the cost factors associated with each. General liability insurance provides coverage for claims of bodily injury, property damage, and personal injury that may occur while conducting business operations. The cost of general liability insurance can vary based on several factors: 1. Industry: The industry in which your business operates plays a significant role in determining your general liability insurance costs. Industries that are considered to be high-risk, such as construction or manufacturing, tend to have higher premiums due to the increased likelihood of accidents and injuries. 2. Business Size and Revenue: The size and revenue of your business are also factors that insurance providers take into consideration. Generally, larger businesses with higher revenues may have higher liability insurance costs, as they have more assets to protect. 3. Claims History: Insurance providers will review your business’s claims history to assess the level of risk associated with insuring your company. If you have a history of frequent claims or costly settlements, it is likely that your general liability insurance costs will be higher. 4. Coverage Limits: The level of coverage you choose for your general liability insurance policy will impact your costs. Higher coverage limits provide more protection but generally come with higher premiums. 5. Location: The location of your business can impact the cost of general liability insurance. Certain states or areas may have higher risks associated with them, such as higher crime rates or natural disasters, which can lead to increased premiums.Factors Affecting Workers Compensation Costs

Workers compensation insurance is specifically designed to provide coverage for employees who suffer work-related injuries or illnesses. The cost of workers compensation insurance can depend on several factors: 1. Employee Classification: Insurance providers take into account the type of work your employees perform and the associated risks. Jobs with higher injury rates, such as construction or manual labor, typically have higher workers compensation costs. 2. Payroll and Employee Count: The size of your workforce and their total payroll can affect the cost of workers compensation insurance. Businesses with more employees or higher payroll amounts will generally have higher premiums. 3. Claims History: Similar to general liability insurance, your business’s claims history also plays a role in determining workers compensation costs. A history of frequent or severe claims can lead to higher premiums. 4. Industry Classification: Different industries have varying levels of risk, and insurance providers use industry classification codes to assign appropriate rates. Higher-risk industries, such as construction or healthcare, typically have higher workers compensation costs. 5. Safety Programs and Practices: Insurance providers consider the safety programs and practices you have in place to mitigate workplace injuries. Businesses with robust safety measures may be eligible for lower workers compensation premiums. In conclusion, understanding the factors that affect the costs of general liability insurance and workers compensation insurance can help you make informed decisions when it comes to safeguarding your business and employees. By assessing these factors and working with an experienced insurance provider, you can ensure that you have adequate coverage at a reasonable cost.Exclusions

When it comes to insurance coverage, understanding the exclusions is crucial for businesses. Both General Liability Insurance and Workers Compensation have specific exclusions that businesses need to be aware of to ensure proper coverage.

Common Exclusions In General Liability Insurance

- Intentional Acts: Coverage does not apply to intentional acts, such as fraud or illegal activities.

- Professional Services: Liability arising from professional services is usually excluded.

- Auto Accidents: General Liability Insurance typically does not cover auto accidents.

Exclusions In Workers Compensation

- Employee Misconduct: Injuries resulting from employee misconduct are generally not covered.

- Self-Inflicted Injuries: Injuries that are self-inflicted by employees are excluded from coverage.

- Preexisting Conditions: Workers Compensation does not cover injuries related to preexisting conditions.

Recommendations

Recommendations:

Choosing The Right Coverage For Your Business

General Liability Insurance safeguards against third-party claims and property damage.

Workers Compensation provides coverage for employees injured on the job.

Evaluate your business needs to determine the most suitable coverage.

Consulting With Insurance Professionals

Seek guidance from experts to get tailored insurance solutions.

Discuss your business specifics for accurate coverage recommendations.

Make informed decisions by consulting with insurance professionals.

Frequently Asked Questions For Is General Liability Insurance The Same As Workers Compensation

Is Workers Compensation The Same As General Liability Insurance?

No, workers’ compensation provides coverage for employees’ medical expenses and lost wages due to work-related injuries, while general liability insurance protects businesses from third-party claims of bodily injury or property damage.

What Does Workers Compensation Insurance Cover?

Workers’ compensation insurance typically covers medical expenses, rehabilitation costs, and a portion of lost wages for employees who are injured on the job.

How Does General Liability Insurance Differ From Workers Compensation?

General liability insurance protects businesses from third-party claims of bodily injury, property damage, and advertising injury, while workers’ compensation provides coverage for work-related injuries and illnesses sustained by employees.

What Are The Key Benefits Of General Liability Insurance For Businesses?

General liability insurance helps protect businesses from legal claims related to third-party bodily injury, property damage, and advertising injury, providing financial protection and peace of mind.

Conclusion

While general liability insurance and workers’ compensation share some similarities, they are not the same. General liability insurance primarily protects businesses from third-party claims, while workers’ compensation covers employees’ work-related injuries or illnesses. Understanding the distinctions between these two types of insurance is crucial for businesses to ensure they have the appropriate coverage in place.

By obtaining both policies, businesses can safeguard their interests and provide a safe working environment for their employees.

Leave a comment