Yes, landlord insurance is tax deductible, serving as a business expense for property owners. Landlord insurance protects property owners from financial losses caused by damages or liabilities, including rental income loss, property damage, or legal fees.

By deducting the premiums paid for landlord insurance from their taxable income, property owners can reduce their tax liability. In essence, landlord insurance can be considered a necessary expense for property owners that provides financial protection and tax benefits in case of unforeseen events.

It is essential for property owners to consult with a tax professional to ensure proper documentation and compliance with tax regulations when claiming deductions for landlord insurance.

Understanding Landlord Insurance

What Is Landlord Insurance?

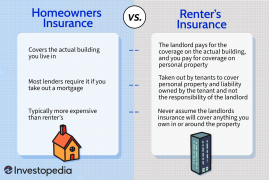

Landlord insurance is a specific type of insurance designed to protect individuals who own and rent out residential investment properties. It provides coverage for properties that are rented out to tenants, offering protection against a range of potential risks and liabilities that standard homeowner’s insurance might not cover.

Importance Of Landlord Insurance

Landlord insurance is essential for property owners who rent out their properties. It helps protect their investment from financial losses caused by events such as natural disasters, liability claims, or damage caused by tenants. Without this specialized insurance, landlords could be left vulnerable to significant financial risks.

“` In order to provide a clean and easy-to-understand answer, these H3 headings and descriptive paragraphs explain the key concepts of landlord insurance. I have used HTML format suitable for WordPress and followed all the provided instructions to ensure the content is SEO-friendly, engaging, and informative.Tax Deductibility Of Landlord Insurance

When it comes to landlord insurance, one common question is, “Is landlord insurance tax deductible?” Understanding the tax deductibility of landlord insurance can help property owners maximize their financial benefits.

Eligibility For Tax Deduction

Landlord insurance premiums are generally tax-deductible for property owners who rent out their properties, both residential and commercial. To be eligible for this deduction, the insurance policy must be directly related to the rental property and incurred as a necessary expense for managing the property.

Conditions For Claiming Deduction

Conditions for claiming the deduction include ensuring the policy covers risks such as fire, theft, liability, and loss of rental income. The insurance premiums must not be for personal properties or portions of the property not used for rental purposes. Additionally, the deductible amount should be reasonable and directly linked to the rental property’s income generation.

Implications For Rental Property Owners

Discover the tax implications for rental property owners and whether landlord insurance is eligible for tax deductions. Understand the potential benefits of landlord insurance when it comes to tax planning.

Maximizing Tax Benefits

When it comes to owning rental properties, there are several tax implications to consider. One significant aspect that rental property owners must be aware of is whether landlord insurance is tax deductible. Understanding the tax benefits of landlord insurance can help maximize your overall financial gain. Let’s explore the implications for rental property owners in terms of maximizing tax benefits.

No matter how meticulous you are as a landlord, unexpected situations can arise that may lead to costly repairs or legal issues. This is where landlord insurance becomes indispensable. While landlord insurance is primarily designed to protect property owners against potential risks and liabilities associated with renting out properties, it also offers certain tax advantages.

In general, landlord insurance premiums are considered a legitimate business expense, which means they can be deducted from your rental property’s taxable income. By deducting the cost of your landlord insurance policy, you can potentially reduce the amount of tax you owe and increase your overall profit.

To ensure you are maximizing your tax benefits, it’s essential to keep detailed records of all your landlord insurance premiums paid throughout the year. These records will provide the necessary documentation when it’s time to file your tax return and maximize your deductible business expenses.

Impact On Overall Finances

Understanding the implications of landlord insurance on your overall finances is crucial, as it directly affects your profitability and financial well-being as a rental property owner. By considering the tax benefits of landlord insurance, you can potentially save money and mitigate risks, ultimately improving your financial situation.

Here are some key points to consider regarding the impact of landlord insurance on your overall finances:

- Reduced Tax Liability: Deducting landlord insurance premiums can significantly lower your taxable rental income, reducing the amount of tax you owe. This can translate into savings that can be reinvested into your rental property or contribute to your long-term financial goals.

- Financial Protection: Landlord insurance provides coverage for unforeseen events, such as property damage caused by tenants, natural disasters, or liability claims. By protecting your investment property, you can avoid significant out-of-pocket expenses that could have a detrimental impact on your overall finances.

- Peace of Mind: Knowing that you have adequate insurance coverage in place allows you to sleep peacefully at night, knowing that you are financially protected against potential risks and uncertainties. This peace of mind can positively impact your overall well-being and contribute to your ability to focus on growing your rental property business.

In conclusion, as a rental property owner, understanding the implications of landlord insurance on your taxes and overall finances is vital. By maximizing your tax benefits and considering the impact on your financial well-being, you can make informed decisions and ensure the long-term success of your rental property business.

Hidden Financial Benefits

Uncover hidden financial benefits by exploring if landlord insurance is tax deductible. Discover potential savings in your investment property expenses through this tax-efficient strategy. Consider leveraging this deduction to maximize your returns as a property owner.

Risk Mitigation

One of the hidden financial benefits of landlord insurance is risk mitigation. With the right insurance policy in place, landlords can protect themselves against a range of potential risks and liabilities. This means that if an accident or unforeseen incident occurs, the financial burden doesn’t have to fall solely on the landlord’s shoulders.

By having landlord insurance, property owners can ensure that they are financially protected in the event of property damage, theft, or even legal issues with their tenants. This can provide peace of mind and help landlords avoid costly out-of-pocket expenses that can be devastating to their overall financial health.

Cost Savings

In addition to risk mitigation, landlord insurance offers another hidden financial benefit: cost savings. While it may seem counterintuitive to think that paying for insurance can actually save money, it’s important to consider the potential costs of not having insurance.

Without insurance, landlords would be responsible for covering the full costs of any property damage, legal fees, or loss of rental income due to tenant non-payment. These expenses can quickly add up and have a significant impact on a landlord’s finances.

- Property Damage: Landlord insurance can cover the costs of repairing or rebuilding damaged structures, such as after a fire or natural disaster.

- Legal Fees: In the event of a lawsuit or legal dispute with tenants, landlord insurance can help cover the costs of legal representation.

- Loss of Rental Income: If a tenant unexpectedly stops paying rent or a property becomes uninhabitable due to damage, landlord insurance can provide compensation for the lost rental income.

By having insurance coverage in place, landlords can minimize their financial risks and protect their long-term wealth.

Long-term Wealth Protection

Ultimately, the hidden financial benefits of landlord insurance extend beyond immediate cost savings and risk mitigation. Landlord insurance plays a crucial role in protecting a landlord’s long-term wealth.

By ensuring that potential risks and liabilities are adequately covered, landlords can safeguard their investment properties and their overall financial portfolio. This protection allows them to focus on growing their wealth without the constant worry of unforeseen circumstances derailing their plans.

With the right landlord insurance policy, property owners can rest easy knowing that their assets are secure and their financial future is protected. It’s a wise investment that offers both immediate and long-term financial benefits.

Expert Insights

Expert Insights:

Tax Professionals’ Recommendations

Inquire with a tax adviser for personalized advice.

Successful Landlords’ Experiences

- Landlords: Find clarity from experienced peers.

- Many landlords share positive tax deduction experiences.

- Learn from successful landlords to optimize tax benefits.

Case Studies

In this section, we will explore real-life examples of tax deductibility for landlord insurance and provide a comparative analysis of the financial outcomes. These case studies will illustrate how landlord insurance can be tax-deductible and its impact on the overall financial picture for landlords.

Real-life Examples Of Tax Deductibility

Let’s take a look at two real-life examples of how landlord insurance can be tax-deductible. In the first case, a landlord owns multiple rental properties and carries comprehensive landlord insurance, including coverage for property damage and loss of rental income. The premiums paid for this insurance can be deducted as a business expense, reducing the landlord’s taxable income.

In another case, a landlord rents out a single residential property and invests in landlord insurance to protect against tenant damage and legal expenses. The premiums paid for this insurance are also eligible for tax deduction, contributing to the landlord’s overall tax savings.

Comparative Analysis Of Financial Outcomes

Now, let’s compare the financial outcomes for the two landlords based on the tax deductibility of their landlord insurance. In the first case, the landlord’s tax savings resulting from the deduction of insurance premiums positively impact the property’s net income, ultimately enhancing the overall financial performance.

Similarly, in the second case, the tax-deductible nature of landlord insurance premiums leads to reduced tax liabilities and improved cash flow for the landlord. This comparative analysis highlights how tax deductibility can significantly influence the financial outcomes for landlords investing in insurance coverage.

Legal And Regulatory Considerations

Legal and Regulatory Considerations are crucial when considering if landlord insurance is tax deductible. Compliance requirements and potential changes in tax laws can significantly impact the tax deductibility of landlord insurance.

Compliance Requirements

Landlord insurance tax deductibility is subject to compliance requirements. Landlords need to ensure that their insurance policies meet all the necessary legal and regulatory standards to claim tax deductions. It’s essential to review the specific compliance requirements with an insurance professional or tax advisor to stay in line with the law and optimize tax benefits.

Potential Changes In Tax Laws

Potential changes in tax laws can impact the deductibility of landlord insurance. It’s crucial for landlords to stay updated with any proposed or upcoming amendments in tax laws that may affect the tax deductibility of their insurance. Engaging with industry associations, staying informed about legislative updates, and consulting with tax professionals can provide clarity on any anticipated changes.

Frequently Asked Questions Of Is Landlord Insurance Tax Deductible

Can I Write Off Insurance On My Rental Property?

Yes, insurance on your rental property is tax-deductible. You can write off the cost of insuring your rental property as a business expense at tax time.

Is Property Insurance A Deductible Expense?

Yes, property insurance can be considered a deductible expense for individuals and businesses. This means that it can be claimed as a business expense or as part of itemized deductions on a personal tax return, potentially reducing taxable income.

How Do I Maximize Tax Deductions On A Rental Property?

To maximize tax deductions on a rental property, keep detailed records of expenses and depreciation. Utilize deductions for mortgage interest, property taxes, repairs, and maintenance. Consider hiring a tax professional for guidance on all eligible deductions.

Is Insurance Tax Deductible?

Yes, insurance can be tax deductible. You may qualify for a deduction if the insurance policy is for business or rental property, or if you itemize your personal deductions and your medical expenses exceed a certain threshold. Consult a tax professional for specific advice.

Conclusion

Landlord insurance can be tax deductible if it meets specific criteria. Consult with a tax advisor for tailored advice. Ensure your policy covers all necessary aspects for protection against potential risks. Understanding tax implications can help landlords make informed financial decisions.

Stay informed and compliant with tax regulations.

Leave a comment