Pension benefits are taxable, although the exact tax treatment depends on the type of pension plan and the recipient’s individual circumstances. In some cases, a portion of the pension may be tax-free, while in other cases, the full amount is subject to taxation.

This can include federal income tax, state income tax, and potentially even additional taxes such as the alternative minimum tax. Therefore, it is important for individuals receiving pension benefits to understand their tax obligations and consult with a tax professional if needed.

Retirement is a significant milestone in one’s life, offering the promise of relaxation and financial security. For most individuals, a part of that security comes in the form of pension benefits, which they have diligently saved and invested in throughout their working years. However, the question of whether these pension benefits are taxable looms over retirees’ heads. The truth is that pension benefits can be subject to taxation, and it is essential to be well-informed about the potential tax implications. We will explore the taxability of pension benefits and shed light on various factors that determine the precise tax treatment for different pension plans and individual circumstances. Understanding the tax obligations associated with pension benefits will help retirees navigate their financial planning effectively and ensure they comply with the tax laws to avoid any unwanted surprises.

:max_bytes(150000):strip_icc()/Term-p-pension-plan-Final-85353401500f4add804371082e83da3a.jpg)

Credit: http://www.investopedia.com

Exploring Pension Benefits

Understanding if pension benefits are taxable is crucial for retirees to plan their finances effectively. Let’s delve into different aspects of pension benefits to gain clarity.

Types Of Pension Plans

There are two main types of pension plans: defined benefit plans and defined contribution plans.

Eligibility Criteria

The eligibility criteria for pension benefits vary based on the specific pension plan and the employer’s policies.

Taxability Of Pension Benefits

Pension benefits are an important source of income for many retirees. However, the taxability of these benefits can be a complex and confusing subject. It’s essential to understand how pension benefits are taxed to effectively plan for your retirement. In this article, we will explore the taxability of pension benefits, focusing on the taxable and nontaxable portions.

Taxable Portion

When it comes to pension benefits, a portion of the income you receive may be subject to federal income tax. The taxable portion of your pension benefits is determined by a few key factors:

- Your age when you started receiving pension payments

- The type of pension plan you have

- Whether any contributions you made to the plan were deducted from your taxes

If you received income tax advantages for your contributions to the pension plan during your working years, it is likely that a portion of your pension benefits will be taxable. This taxable amount is then treated as ordinary income and is subject to the regular tax rates based on your tax bracket.

Nontaxable Portion

While a portion of your pension benefits may be taxable, it’s important to note that some parts may be nontaxable. The nontaxable portion typically consists of the contributions you made to the plan that were already taxed.

For example, if you contributed to a pension plan with after-tax dollars, that portion of your benefits is generally not subject to federal income tax. The nontaxable portion is excluded from your taxable income calculation, reducing your overall tax liability.

It’s worth mentioning that if you made contributions to a pension plan with both pretax and after-tax dollars, the overall taxability of your benefits may be more complex. In such cases, the Internal Revenue Service (IRS) typically utilizes a formula to determine the taxable and nontaxable portions.

In conclusion, the taxability of pension benefits depends on various factors such as your age, the type of pension plan, and the contributions you made. Understanding the taxable and nontaxable portions of your benefits is crucial for effective retirement planning. By knowing how your pension benefits will be taxed, you can make informed decisions to optimize your retirement income.

Factors Influencing Taxation

Pension benefits may be taxable depending on various factors, such as the type of pension plan and the recipient’s income level. Factors influencing taxation include the source of the pension income, the recipient’s age, and any contributions made before retirement.

It is important to consult with a tax professional for accurate advice on the taxability of pension benefits.

Factors Influencing Taxation As you consider pension benefits, it’s crucial to understand the various factors that can impact the taxation of these funds. Two significant factors that influence the taxability of pension benefits include the age of the pensioner and the source of the funds. Let’s delve into these influencing factors. “`htmlAge Of The Pensioner

“` The age at which a pensioner begins receiving benefits can have a substantial impact on the tax treatment of those funds. Individuals who receive pension benefits before reaching the age of 59½ may be subject to an early withdrawal penalty, in addition to the regular income tax. On the other hand, those who commence receiving pension funds after this age may not incur the early withdrawal penalty. “`htmlSource Of Funds

“` The tax treatment of pension benefits can also be influenced by the source of the funds. Pension benefits stemming from contributions made with after-tax dollars are typically not subject to additional taxation. Conversely, funds derived from pre-tax contributions or employer contributions, such as those from traditional 401(k) plans, are generally taxable upon distribution. In summary, the age of the pensioner and the source of the funds are crucial factors that can significantly impact the taxation of pension benefits. Understanding these influences can aid individuals in making informed decisions regarding their retirement income.

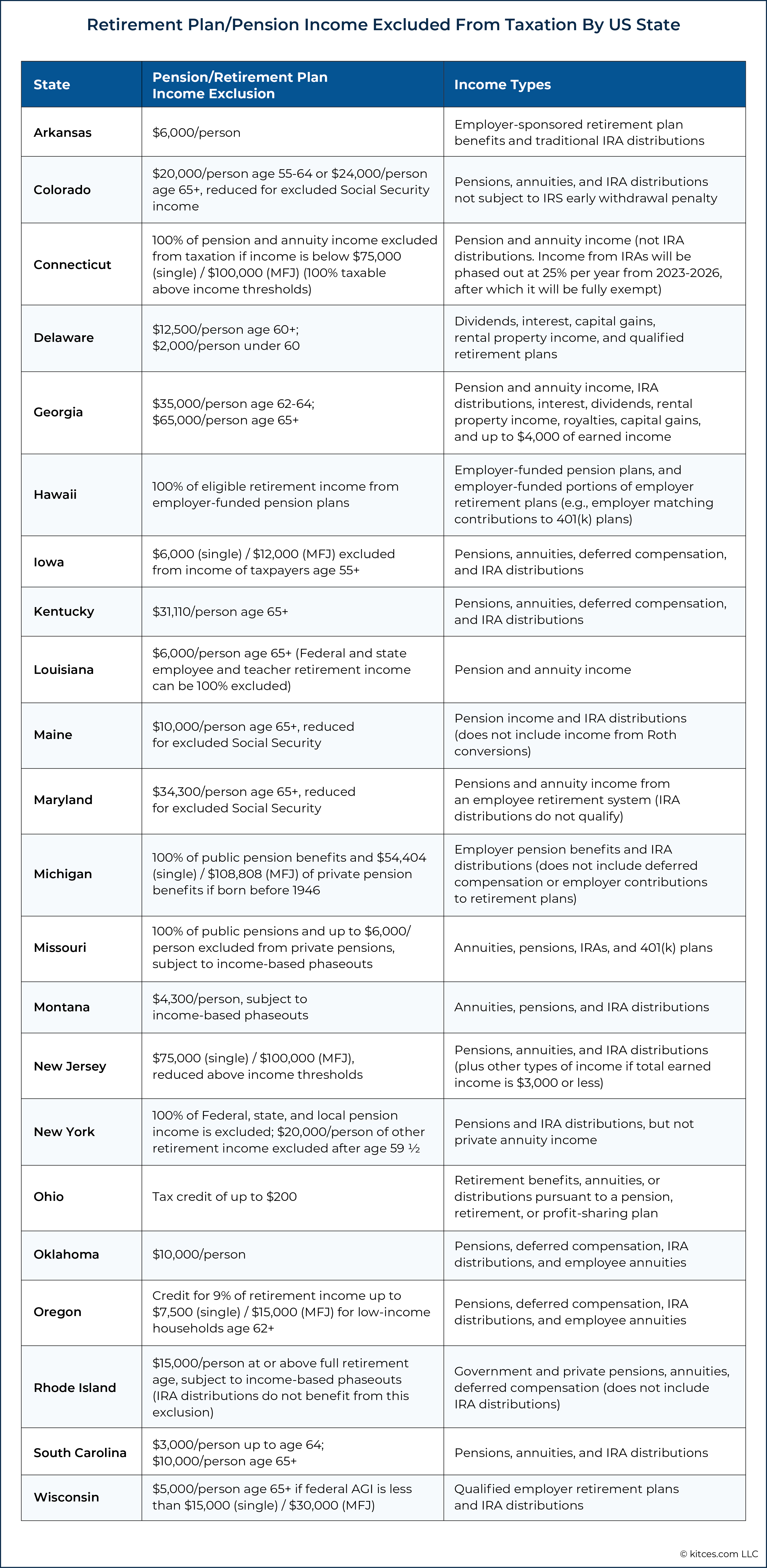

Credit: http://www.kitces.com

Tax Treatment Of Different Pension Plans

When it comes to retirement planning, understanding the tax treatment of different pension plans is crucial. Different pension plans have differing tax implications, which can significantly impact your retirement income. Knowing how your pension benefits are taxed is essential for effective financial planning.

Defined Benefit Plans

Defined benefit plans provide retirees with a predetermined monthly payment based on a formula considering the employee’s salary history and years of service. The tax treatment of defined benefit plans is such that the amount you receive is generally subject to federal income tax, and in some instances, state income tax as well. These payments are taxable in the year you receive them, regardless of whether they are disbursed as a lump sum or in periodic installments.

Defined Contribution Plans

Unlike defined benefit plans, which provide a fixed amount, defined contribution plans, such as 401(k) or 403(b), are tax-deferred retirement accounts. Contributions to these plans are made pre-tax, reducing your taxable income in the year of contribution. However, when you withdraw funds from a defined contribution plan during retirement, the amount withdrawn is subject to federal and potentially state income tax. This tax treatment is applicable whether the distribution is taken as a lump sum or as periodic payments.

Potential Tax Deductions

Unravel the mystery of taxable pension benefits and potential tax deductions for a clearer financial outlook. Understanding the nuances can lead to significant savings and smarter financial planning. Maximize your tax benefits by grasping the tax implications of pension benefits.

Contributions To The Plan

If you’re wondering if pension benefits are taxable, you’ll be pleased to know that potential tax deductions could work in your favor. One of the most notable deductions is related to contributions made to the pension plan.

When you contribute to a pension plan, your contributions are typically tax-deductible. This means that you can reduce your taxable income by the amount you contribute to your retirement savings. It’s like giving yourself a financial boost while also strengthening your retirement security.

In order to take advantage of this tax deduction, there are certain criteria you need to meet. First, your contributions must be made to a qualified plan, such as a 401(k) or an individual retirement account (IRA). Additionally, your contributions must fall within the limits set by the Internal Revenue Service (IRS). These limits may vary depending on your age, the type of plan, and other factors. Always consult with a tax professional to ensure you are following the guidelines and maximizing your deductions.

Healthcare Expenses

Another potential tax deduction that can bring some relief when it comes to pension benefits is related to healthcare expenses. As we age, medical costs tend to increase, and these expenses can take a toll on our retirement income. However, the tax code does offer some relief in this area.

If you itemize your deductions, you may be eligible to deduct certain healthcare expenses as part of your medical deductions. These expenses include medical and dental expenses, as well as premiums paid for long-term care insurance.

It’s important to note that there are certain restrictions and requirements you must meet in order to qualify for these deductions. For example, only expenses that exceed a certain percentage of your adjusted gross income (AGI) can be deducted. The IRS sets this threshold, which is subject to change year by year.

Keep in mind that keeping track of healthcare expenses can be time-consuming, so it’s advisable to maintain organized records and receipts. It’s also a good idea to consult with a tax professional to ensure you are taking full advantage of the deductions available to you.

Tax Reporting And Withholding

A Form 1099-R reports distributions from pensions, annuities, retirement or profit-sharing plans, IRAs, insurance contracts, etc.

Taxpayers can opt for voluntary tax withholding on pension benefits by specifying the amount they want withheld.

State Tax Considerations

When it comes to pension benefits, understanding state tax considerations is crucial for proper financial planning.

State Tax Regulations

State tax regulations play a significant role in determining whether pension benefits are taxable in a specific location.

State-specific Exemptions

Some states offer exemptions on pension benefits, providing tax relief for retirees in those areas.

Consulting a tax advisor is advisable to navigate state tax regulations effectively.

Understanding state-specific exemptions can help retirees maximize their retirement income.

Credit: fastercapital.com

Seeking Professional Advice

When it comes to understanding if pension benefits are taxable, seeking professional advice is crucial. Consulting with a tax professional will provide you with personalized insights and guidance tailored to your specific financial situation.

Consulting A Tax Professional

Consulting a tax professional is a pivotal step in gaining clarity on the tax implications of your pension benefits. An experienced tax advisor can assess your unique circumstances and provide strategic advice on how to minimize tax liabilities while maximizing your retirement savings.

Utilizing Retirement Calculators

Furthermore, utilizing retirement calculators can help you estimate the tax implications of your pension benefits. These tools allow you to input various financial scenarios and retirement income sources to forecast your tax obligations in retirement.

Frequently Asked Questions Of Is Pension Benefits Taxable

Is Pension Income Taxable?

Pension income is generally taxable at the federal and possibly state level. The tax treatment depends on various factors, including the type of pension plan and your total income.

How Are Pension Benefits Taxed?

Pension benefits are typically taxed as ordinary income. This means they are subject to the same tax rates as other sources of income, such as wages or salaries. The specific tax treatment can vary based on the type of pension plan and individual circumstances.

Are Social Security Benefits Taxable?

In some cases, a portion of your Social Security benefits may be taxable, depending on your total income and filing status. The IRS uses a formula to determine the taxable amount, and up to 85% of your benefits could be subject to income tax.

What Is The Tax Rate On Pension Income?

The tax rate on pension income varies based on your total income, filing status, and other specific circumstances. It is essential to consult with a tax professional to understand the exact tax implications of your pension benefits.

Conclusion

Based on the information presented, it is clear that pension benefits can indeed be taxable. It is important for individuals to understand the various factors that may determine if and how much of their pension income is subject to taxation.

Consulting with a tax professional or financial advisor can provide valuable insights and guidance in navigating this complex aspect of retirement planning. Being aware of the tax implications of pension benefits can help individuals make informed decisions and effectively manage their finances in retirement.

Leave a comment