Pension fund contribution refers to the amount of money or assets that an individual or employer contributes to a pension fund. It is a financial commitment made to ensure future retirement benefits for the individual.

Pension funds are typically managed by third-party administrators who invest the contributions to generate returns over time. These returns, along with the contributions, form the pension fund balance that is used to provide income during retirement. The contribution amount can be a fixed percentage of the employee’s salary or a specified amount determined by the employer.

Regular contributions to a pension fund are essential for building a sufficient retirement corpus and ensuring financial security in one’s later years.

Credit: http://www.theglobeandmail.com

Importance Of Pension Fund Contribution

Understanding the significance of pension fund contribution is crucial for ensuring financial stability in retirement.

Tax Benefits Of Pension Contributions

By contributing to a pension fund, individuals can benefit from tax advantages, reducing their tax liabilities.

Security In Retirement

Contributing to a pension fund provides a secure financial foundation for retirement, ensuring a comfortable lifestyle.

Types Of Pension Funds

When it comes to pension funds, there are various types that individuals and organizations can choose from. Each type has its own distinctive features and benefits. Understanding these types can help you make an informed decision about which pension fund is right for you. In this section, we will explore the three most common types of pension funds: Defined Benefit Plans, Defined Contribution Plans, and Hybrid Plans.

Defined Benefit Plans

Defined Benefit Plans, sometimes referred to as traditional pension plans, provide a fixed amount of retirement income to employees based on a predetermined formula. These plans are typically funded by the employer, who contributes a specific percentage of the employee’s salary throughout their working years.

In a Defined Benefit Plan, the employee’s retirement benefit is determined by factors such as years of service and final average salary. This means that the longer an employee works for an organization and the higher their salary at retirement, the greater their pension benefit will be.

One of the advantages of Defined Benefit Plans is the security they provide, as the retirement income is guaranteed regardless of how the pension fund performs. However, these plans put the financial burden on the employer, who is responsible for ensuring there are enough funds to meet the future benefit obligations.

Defined Contribution Plans

Defined Contribution Plans, also known as individual account plans, differ from Defined Benefit Plans as the retirement income is based on the contributions made to the employee’s account and the investment performance of those contributions.

In a Defined Contribution Plan, both the employer and the employee can contribute to the retirement account. The employer may offer a matching contribution up to a certain percentage of the employee’s salary. The employee has control over the investment decisions within the plan, selecting from a range of investment options offered by the plan.

One of the key advantages of Defined Contribution Plans is the portability they offer. Since the account belongs to the employee, it can be transferred if they change jobs. Additionally, these plans provide employees with the opportunity to grow their retirement savings through investment returns.

Hybrid Plans

Hybrid Plans, as the name suggests, combine features of both Defined Benefit and Defined Contribution Plans. These plans aim to offer the advantages of both types while mitigating their drawbacks.

One popular type of Hybrid Plan is the Cash Balance Plan, where the employer contributes a fixed percentage of the employee’s salary into an individual account. The account grows with interest credits, similar to a Defined Benefit Plan, but the employee has more transparency and control over their account balance.

Another type of Hybrid Plan is the Target Benefit Plan, which defines a target retirement benefit, similar to a Defined Benefit Plan. However, the contributions made by the employer and the employee are based on a formula to ensure that the plan remains adequately funded, similar to a Defined Contribution Plan.

Hybrid Plans provide flexibility and a balance between guaranteed benefits and individual control. They offer employees the opportunity to build retirement income while still providing some level of security.

Calculating Pension Fund Contribution

Calculating pension fund contributions is an essential aspect of retirement planning. Pension fund contribution refers to the percentage of an employee’s salary that is set aside for their future retirement benefits. It is important for both employers and employees to understand how these contributions are calculated and the various strategies that can optimize their retirement savings.

Employer Matching Contributions

Employer matching contributions are a vital part of pension fund contributions. These contributions involve the employer matching a percentage of the employee’s contribution to the pension fund. For example, if an employee contributes 3% of their salary to the pension fund, the employer may match this amount, effectively doubling the employee’s contribution. This matching contribution can significantly boost the employee’s retirement savings.

Personal Contribution Strategies

Developing effective personal contribution strategies is crucial for maximizing retirement savings. Employees can choose to contribute a specific percentage of their salary to the pension fund, aligning with their long-term financial goals. They can also explore additional voluntary contribution options to further bolster their retirement savings. By strategically managing their contributions, individuals can ensure a secure and comfortable retirement.

Strategies To Maximize Pension Fund Contributions

Increase Contribution Percentage

Elevating percentage boosts long-term retirement savings.

Catch-up Contributions

Over 50? You can make additional catch-up contributions.

Utilizing Tax-advantaged Accounts

A type of account giving tax benefits for retirement savings.

Common Mistakes To Avoid

When it comes to pension fund contributions, it’s essential to understand the common mistakes that people often make. Avoiding these mistakes can help you make the most of your retirement savings in the long run.

Not Taking Full Advantage Of Employer Match

If your employer offers a matching contribution to your pension fund, failing to take full advantage of this benefit can mean leaving money on the table. Make sure to maximize your contributions to meet the employer’s match to secure the full advantage of this opportunity.

Underestimating Retirement Needs

Underestimating the amount of money you will need in retirement can lead to financial hardship later on. It’s important to carefully calculate your future expenses and plan accordingly to ensure you have enough funds to support your retirement lifestyle.

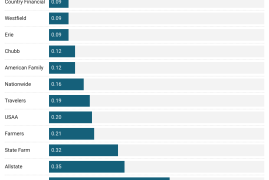

Credit: http://www.pensiondeductions.com

Impact Of Pension Fund Contributions On Retirement Lifestyle

Contributing to a pension fund can significantly impact one’s retirement lifestyle. The regular pension fund contributions made during one’s working years play a crucial role in ensuring a comfortable and financially stable retirement.

Financial Security In Retirement

Pension fund contributions provide a steady income stream for retirees, offering financial security and peace of mind during their golden years.

Ability To Pursue Hobbies And Travel

By contributing to a pension fund, retirees can maintain their lifestyle and have the financial freedom to pursue hobbies, travel, and enjoy leisure activities without worrying about financial constraints.

Role Of Financial Advisors In Pension Planning

In the world of pension planning, financial advisors play a crucial role in helping individuals make informed decisions about their pension fund contributions. As trusted experts in the field, these advisors provide valuable guidance and assistance in creating effective contribution strategies, monitoring and adjusting contribution plans, and ultimately ensuring a secure retirement.

Expert Advice On Contribution Strategies

When it comes to pension fund contributions, financial advisors are well-versed in various strategies that can help maximize returns and ensure a comfortable retirement. They analyze your financial situation, taking into account factors such as your age, income, and risk tolerance to devise a contribution plan that suits your needs. Their expert advice can guide you in determining the optimal amount to contribute and assist in aligning your goals with your financial capabilities.

Monitoring And Adjusting Contribution Plans

Financial advisors also play a crucial role in monitoring and adjusting your pension fund contribution plan over time. They understand that life circumstances can change, and as such, your contribution plan may need to be adjusted accordingly. Advisors regularly review your investment portfolio, making sure it is performing as expected and making necessary changes when market conditions require. By staying proactive and continuously monitoring your contribution plan, they can help optimize your investment returns and ensure that you remain on track to reaching your retirement goals.

Financial advisors are familiar with the ever-changing laws and regulations that govern pension planning. They stay up to date with the latest industry trends and changes, providing valuable insights to help you navigate the complex landscape of retirement planning. With their guidance, you can make sound decisions regarding your pension fund contributions, ensuring a secure and comfortable retirement future.

Credit: fastercapital.com

Moving Forward: Creating A Sustainable Retirement Plan

When it comes to planning for retirement, it is essential to create a sustainable retirement plan that will support you in your later years. One of the key elements of such a plan is understanding and maximizing your pension fund contribution. Your pension fund contribution consists of the money you set aside from your earnings during your working years to ensure a steady income during retirement. In this article, we will explore how you can move forward and create a sustainable retirement plan by diversifying your retirement investments and regularly reviewing your retirement goals.

Diversifying Retirement Investments

One of the most effective ways to create a sustainable retirement plan is by diversifying your retirement investments. This means investing your pension fund contributions in a variety of assets such as stocks, bonds, real estate, and mutual funds. By spreading your investments across different asset classes, you can mitigate the risk of losing all your retirement savings due to the fluctuation of a single investment.

Diversification helps to achieve a balance between risk and reward. It allows you to potentially earn higher returns while minimizing the impact of market volatility. For example, if the stock market takes a downturn, your other investments such as bonds or real estate might still perform well, providing stability to your retirement income.

Regularly Reviewing Retirement Goals

In addition to diversifying your retirement investments, it is crucial to regularly review your retirement goals. As you progress through your career and life, your retirement needs and aspirations may change. Therefore, it is essential to adjust your pension fund contribution and investment strategy accordingly to align with your evolving goals.

Regularly reviewing and updating your retirement goals allows you to stay on track and make necessary adjustments to your savings and investments. For example, if you find that your current pension fund contribution is not sufficient to meet your desired retirement lifestyle, you may need to increase your contributions or explore additional investment opportunities. On the other hand, if you are ahead of your retirement goals, you might consider reducing your contributions and reallocating the funds to other financial priorities.

Taking the time to review and reassess your retirement goals ensures that you are always working towards creating a sustainable retirement plan that aligns with your changing circumstances and aspirations.

Frequently Asked Questions Of What Is Pension Fund Contribution

What Is A Pension Fund Contribution?

A pension fund contribution is a regular payment made to a pension fund by both the employer and the employee. It is designed to provide income for employees post-retirement. The money contributed grows over time, typically through investment, to provide a source of income during retirement.

Why Is Pension Fund Contribution Important?

Pension fund contributions are important because they help individuals save for retirement. By making regular contributions, individuals can build a substantial fund that will provide financial security during their later years. Additionally, pension fund contributions often come with tax benefits, making them a valuable long-term investment option.

How Does Pension Fund Contribution Work?

Pension fund contributions work by setting aside a portion of an employee’s salary each month, along with a corresponding contribution from the employer. These funds are then invested in a variety of assets to grow over time. Upon retirement, the accumulated amount is used to provide regular income to the individual.

Can I Change The Amount Of My Pension Fund Contribution?

Yes, you can change the amount of your pension fund contribution. Many pension plans allow participants to change their contribution amount at specified intervals, such as annually or upon a qualifying life event. It’s important to review your plan’s guidelines to understand how and when changes can be made.

Conclusion

Understanding pension fund contribution is crucial for securing a stable financial future. It allows individuals to set aside funds during their earning years to ensure a comfortable retirement. By contributing regularly, one not only builds a retirement nest egg but also benefits from employer matching contributions and potential tax advantages.

Planning for retirement should be a top priority, and pension fund contribution is an effective way to achieve that goal. Start saving for the future today!

Leave a comment