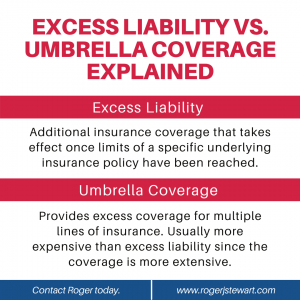

Personal Umbrella Excess Insurance is additional liability coverage that provides protection beyond the limits of your primary insurance policies. It offers extra financial security to individuals in case they are involved in an accident or face a lawsuit where the costs exceed their underlying coverage.

This type of insurance can cover various aspects, such as bodily injury, property damage, and even legal fees. With Personal Umbrella Excess Insurance, you can have peace of mind knowing that you have additional protection against unexpected events and potentially costly claims.

It acts as a safety net, bridging the gap between your existing insurance policies and any potential financial risks you may face.

Credit: http://www.insurancecentermo.com

Benefits

Personal Umbrella Excess Insurance provides additional coverage beyond standard policies, protecting against unforeseen circumstances and offering increased financial security. This type of insurance offers high liability limits that extend coverage for various liability risks, giving individuals further peace of mind.

First things first, let’s delve into the benefits of Personal Umbrella Excess Insurance.Enhanced Liability Protection

Personal Umbrella Excess Insurance provides an extra layer of financial security and peace of mind, ensuring you are safeguarded against unexpected costs beyond what your primary policies cover.

Coverage Extensions

- Expand your coverage for situations where your Home, Auto, or Boat insurance may fall short.

- Protect your assets from legal liabilities stemming from accidents or unforeseen events.

- Obtain additional coverage for legal defense fees and settlements, giving you a comprehensive safety net.

Coverage Details

Personal Umbrella Excess Insurance provides additional liability coverage beyond standard policy limits. It safeguards against financial loss due to unforeseen events, offering extended protection for personal assets. This coverage detail ensures comprehensive security and peace of mind.

Limits And Scope Of Protection

Personal Umbrella Excess Insurance offers coverage beyond the limits of your basic insurance policies. It acts as an additional layer of protection to safeguard your assets and future earnings from unforeseen circumstances. Unlike regular insurance policies that have predefined coverage limits, a personal umbrella policy provides much higher coverage limits that can range from $1 million to $10 million or more. This ensures that you have substantial financial protection in case of a large claim or lawsuit that exceeds your primary insurance coverage limits. With a personal umbrella policy, you get an extended scope of protection that goes above and beyond what your primary insurance policies cover. It provides coverage for various types of incidents that may occur in your day-to-day life, giving you peace of mind and a sense of security.Types Of Incidents Covered

Personal umbrella insurance covers a wide range of incidents, including but not limited to:- Automobile accidents: If you are involved in a car accident where you are at fault and the damages or injuries exceed the limits of your auto insurance policy, your umbrella policy will step in to cover the remaining expenses.

- Home accidents: If someone gets injured on your property and decides to sue you for damages, your umbrella policy will protect you from potential financial ruin by covering legal expenses and compensation.

- Libel or slander accusations: In today’s interconnected world, it’s easier than ever for someone to make false claims about you or your business. If you find yourself facing a defamation lawsuit, your personal umbrella policy can provide coverage for legal defense costs and any potential settlements.

- Personal injury lawsuits: If you unintentionally injure someone or cause damage to their property, and they decide to sue you for compensation, your umbrella policy will offer additional coverage beyond what your basic liability insurance provides.

- Legal defense costs: Personal umbrella insurance also includes coverage for legal defense costs, such as attorney fees, court costs, and other expenses associated with defending yourself in a lawsuit.

- Other incidents: Personal umbrella insurance covers a wide array of incidents, including accidents involving boats or other recreational vehicles, incidents that occur during international travel, and even false arrest or malicious prosecution claims.

Policy Considerations

When considering personal umbrella excess insurance, it’s important to take into account various policy considerations. Understanding the underlying coverage requirements, as well as the exclusions and limitations, plays a critical role in ensuring comprehensive protection. Here’s what you need to know:

Underlying Coverage Requirements

Before securing a personal umbrella excess insurance policy, it’s essential to evaluate the underlying coverage requirements. Typically, insurers mandate specific minimum liability limits for primary policies, such as auto or homeowners insurance. These underlying policies must meet the designated threshold to be eligible for umbrella coverage. Failure to maintain the required underlying coverage may result in gaps in protection and the potential claim denial by the umbrella insurer.

Exclusions And Limitations

Understanding the exclusions and limitations of a personal umbrella excess insurance policy is crucial. While this coverage provides an additional layer of protection, it’s important to be aware that certain scenarios may be excluded from coverage. These exclusions could include intentional acts, injuries related to business activities, or claims exceeding the policy limits. Furthermore, limitations on coverage for specific types of property or legal actions may apply, necessitating a thorough review of the policy terms and conditions.

Credit: http://www.ioausa.us

Costs And Premiums

Understanding the costs and premiums of Personal Umbrella Excess Insurance is crucial in making informed decisions about protecting your assets and finances. By delving into the factors affecting premiums and conducting a comparative analysis, you can gain a clearer insight into the pricing structure and offerings of this important form of insurance.

Factors Affecting Premiums

Several key factors impact the premiums associated with Personal Umbrella Excess Insurance. These include the policyholder’s risk profile, coverage limits, prior claims history, underlying insurance policies, geographic location, and the insurance carrier’s pricing strategy.

- Policyholder’s risk profile

- Coverage limits

- Prior claims history

- Underlying insurance policies

- Geographic location

- Insurance carrier’s pricing strategy

Comparative Analysis

When selecting a Personal Umbrella Excess Insurance policy, conducting a thorough comparative analysis is essential for evaluating coverage options and costs from different insurance providers. This process involves examining premium rates, coverage limits, deductibles, and additional benefits offered by each policy, enabling you to make a well-informed decision.

When Is A Personal Umbrella Excess Policy Needed?

Personal umbrella excess insurance provides an extra layer of liability protection beyond the limits of your underlying insurance policies. But how do you determine if you need it? One way is by assessing your personal risk factors. For example, if you have a high net worth, own valuable assets, or engage in activities that pose a higher risk of injury or property damage, a personal umbrella excess policy is crucial to safeguarding your financial future.

Here are a few personal risk factors to consider:

- Your income level: Individuals with high incomes should consider a personal umbrella excess policy to protect their financial stability if faced with a significant lawsuit or liability claim.

- The value of your assets: If you own valuable assets such as property, vehicles, or even artwork, having a personal umbrella excess policy ensures that your assets are adequately protected in case of a lawsuit or accident.

- Your lifestyle and hobbies: Do you frequently entertain guests at your home? Do you participate in high-risk activities like boating, skiing, or skydiving? If so, you may be exposing yourself to a higher chance of liability claims, making a personal umbrella excess policy a wise investment.

- Your profession: Certain professions, such as doctors, lawyers, or business owners, are more prone to liability claims. If you work in a profession with a higher risk of potential lawsuits, a personal umbrella policy can provide the added protection you need.

When considering a personal umbrella excess policy, it’s important to take into account your assets and income. The extent of your assets and income can greatly influence the amount of coverage you should have. Here’s how:

| Assets | Recommended Coverage |

|---|---|

| Less than $1 million | $1 million |

| $1 million – $5 million | $2 million |

| Over $5 million | $5 million or more |

For example, if you have assets worth $3 million, it is recommended to have at least a $2 million personal umbrella excess policy. Your income level also plays a role in determining the coverage you need. Consider your potential future earnings and the impact a significant liability claim could have on your financial stability.

In summary, a personal umbrella excess policy is needed when you have significant personal risk factors such as a high net worth, valuable assets, or engage in high-risk activities. Assessing these risk factors, as well as considering your income and assets, will help you determine the appropriate coverage for your personal umbrella excess policy.

Choosing The Right Coverage

`Consider `Personal Umbrella Excess Insurance` to safeguard yourself from unforeseen risks beyond regular coverage limits.`

`selecting Adequate Policy Limits`

`Evaluate your current assets and potential liabilities when determining the optimal policy limits for your `Personal Umbrella Excess Insurance`.`

`additional Policy Features`

`Look for `additional features` such as coverage for legal fees and worldwide protection when exploring `Personal Umbrella Excess Insurance` options.`

:max_bytes(150000):strip_icc()/Commercial-General-Liability-Final-51e0c0f9b27d4e409a7f49da59fbe037.jpg)

Credit: http://www.investopedia.com

Frequently Asked Questions For What Is Personal Umbrella Excess Insurance

What Is Personal Umbrella Excess Insurance?

Personal Umbrella Excess Insurance provides additional liability coverage beyond the limits of your existing policies. It offers protection against lawsuits resulting from property damage, bodily injury, defamation, and other personal liabilities. It is designed to safeguard your assets in the event of a major claim.

Who Needs Personal Umbrella Excess Insurance?

Anyone with substantial assets or a high-risk profession may benefit from this coverage. It is especially important for individuals with significant wealth, multiple properties, high-profile careers, or high liability risks. In today’s litigious society, having this extra layer of protection can provide peace of mind and financial security.

How Does Personal Umbrella Excess Insurance Work?

If you are sued for damages exceeding the liability limits of your homeowners or auto insurance, your umbrella policy kicks in to cover the additional costs. It acts as a safety net, helping to protect your savings, investments, and valuable assets.

This coverage can be crucial in situations of devastating accidents or legal claims.

What Are The Benefits Of Personal Umbrella Excess Insurance?

This coverage offers extensive protection at a relatively low cost. It can safeguard your assets, future earnings, and standard of living. Additionally, it provides peace of mind by offering higher liability limits, coverage for various unforeseen events, and legal defense costs.

In essence, it offers an added layer of security for you and your family.

Conclusion

Personal umbrella excess insurance provides additional liability protection beyond the limits of your existing policies. It safeguards you against the financial risks that arise from unforeseen accidents or incidents. By securing this insurance, you can protect your assets and ensure peace of mind.

With the increasing complexity of legal issues, personal umbrella excess insurance becomes even more crucial. Don’t wait until it’s too late – consider getting this essential coverage today. Keep yourself protected and enjoy life without worry.

Leave a comment