Landlord insurance typically expires annually, needing renewal to maintain property coverage and protection. As a property owner, understanding the expiry date of your landlord insurance is crucial for ensuring continuous safeguarding of your investment.

When your landlord insurance expires, your property may be vulnerable to potential risks such as damage, liability claims, or loss of rental income. It is essential to stay proactive and stay on top of your insurance renewal dates to avoid any gaps in coverage that could lead to financial losses or legal issues.

By renewing your landlord insurance on time, you can mitigate risks and protect your property investment effectively.

Understanding Landlord Insurance

Landlord insurance provides coverage for damages and liabilities, but it’s essential to stay mindful of when your policy expires. Once your landlord insurance expires, you risk financial losses and potential legal issues if unforeseen events occur. It’s crucial to renew your policy in a timely manner to maintain protection for your property.

What Is Landlord Insurance?

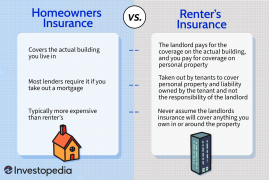

Landlord insurance is a type of insurance policy designed to protect individuals who own rental properties. It typically provides coverage for the building itself, as well as liability protection and coverage for loss of rental income.

Importance Of Landlord Insurance

Landlord insurance is vital for protecting landlords from financial losses. In the event of unforeseen circumstances such as property damage, rental defaults, or legal disputes, having landlord insurance can provide financial security.

Expiration Of Landlord Insurance

Introduction:When Landlord Insurance Expires, it’s crucial to understand the implications and risks associated if you do not renew the coverage in time. Let’s delve into the potential consequences of expired insurance policies for landlords.

Implications Of Expired Insurance:

Failure to renew landlord insurance could lead to financial loss and legal complications.

Risks Faced Without Insurance Coverage:

Without insurance, landlords are exposed to liabilities from property damage and lawsuits.

Assessing Your Property And Risks

When it comes to protecting your property investment, renewing your landlord insurance before it expires is crucial. However, it is equally important to assess your property and risks to ensure you have the right coverage in place. By evaluating your property and identifying potential risks, you can make informed decisions that protect your investment and give you peace of mind.

Evaluation Of Property

Before renewing your landlord insurance, it is essential to conduct a thorough evaluation of your property. This evaluation helps you understand the current condition of your property and identify any areas that require attention or improvement.

Here are a few key factors to consider when evaluating your property:

- Physical condition of the property, including any existing damages or maintenance issues.

- Age and quality of the building materials used in construction.

- Structural integrity, including the foundation, roof, and walls.

- Security measures in place, such as locks, alarms, and surveillance systems.

- Accessibility and safety features, including fire escapes, handrails, and smoke detectors.

- Energy efficiency and sustainability features, which can impact insurance premiums.

By thoroughly evaluating your property, you can not only address any existing issues but also take proactive steps to minimize potential risks.

Identifying Potential Risks

Identifying potential risks is an essential part of assessing your property and ensuring adequate insurance coverage. By understanding the specific risks associated with your property, you can customize your insurance policy to provide comprehensive protection.

Consider the following potential risks:

- Location hazards, such as being in a high-crime area or prone to natural disasters.

- Occupancy risks, such as renting to tenants with a history of property damage or non-payment of rent.

- Property-specific risks, including the presence of swimming pools, trampolines, or other high-liability features.

- Liability risks for common areas, such as parking lots or shared facilities.

- Legal and financial risks, such as lawsuits, eviction costs, or loss of rental income due to damages.

By identifying these potential risks, you can work with your insurance provider to ensure your policy covers them adequately. This proactive approach helps protect you from unexpected financial burdens and ensures peace of mind.

Renewing Or Finding New Coverage

When the expiration date of your current landlord insurance policy approaches, you need to make an important decision: should you renew your existing coverage or start searching for a new insurance provider? Both options have their advantages and it’s crucial to evaluate them thoroughly to ensure you make the best choice for your needs. Let’s explore the options for renewal and the steps involved in searching for new insurance.

Options For Renewal

Renewing your landlord insurance policy with your current provider can be a simple and time-saving option. It allows you to maintain the same level of coverage without the hassle of searching for a new insurance company. However, before automatically renewing your policy, take a moment to consider the following:

- Review the coverage and deductibles of your current policy to ensure they still meet your needs.

- Contact your insurance provider to discuss any changes in your circumstances or property that may require adjustments to your policy.

- Compare the renewal premium with quotes from other insurance companies to ensure you are getting the best value for your money.

By carefully evaluating your options for renewal, you can make an informed decision about continuing with your current insurance provider or exploring other alternatives.

Searching For New Insurance

If you decide to search for new insurance coverage, there are several steps you can follow to help simplify the process:

- Assess your insurance needs: Consider the specific requirements of your rental property and the level of coverage you desire. This will help you narrow down the types of insurance policies you should be looking for.

- Gather necessary information: Prepare the details of your rental property, such as its location, size, and condition. Additionally, gather any relevant documentation, such as past claims history and rental income information.

- Get multiple quotes: Reach out to different insurance companies and request quotes for landlord insurance. Make sure to provide the same information to each company so you can compare the quotes accurately.

- Evaluate coverage and terms: Review the coverage and policy terms of each quote you receive. Pay close attention to the limits, exclusions, and deductibles to ensure they meet your specific needs.

- Consider customer reviews and reputation: Research the reputation of the insurance companies you are considering. Look for customer reviews and ratings to gauge their reliability and customer service.

- Make an informed decision: Based on the quotes, coverage, and reputation of the insurance companies, choose the one that provides the best value and suits your requirements.

Searching for new insurance can be time-consuming, but it can also lead to better coverage and potentially save you money. Take the necessary steps to find the insurance company that offers the right combination of coverage, price, and service.

Legal And Financial Implications

Legal and Financial Implications:

Understanding Legal Obligations

Renting out property comes with specific legal responsibilities for landlords.

Landlord insurance is more than a helpful tool; it fulfills legal requirements.

Without insurance, landlords may face legal consequences in case of incidents.

Financial Impact Of Lapse In Coverage

A lapse in insurance coverage can have severe financial repercussions for landlords.

Landlords would bear the full financial burden in case of damage or liability.

Reinstating insurance after a lapse can lead to higher premiums and deductibles.

Implementing Risk Mitigation Strategies

When landlord insurance expires, implementing risk mitigation strategies becomes crucial. Protecting your property and minimizing potential losses through proactive measures is essential. Seeking alternative insurance options or implementing stricter tenant screening can help mitigate risks associated with an expired landlord insurance policy.

Implementing Risk Mitigation Strategies Temporary Risk Management Measures Implementing temporary risk management measures is crucial when landlord insurance expires. During this time, landlords should prioritize the security and safety of their rental properties. Temporary risk management measures can include installing security cameras, conducting regular property inspections, and increasing communication with tenants to address any concerns promptly. Long-Term Risk Protection For long-term risk protection, landlords should consider investing in robust landlord insurance coverage. This can include comprehensive policies that cover property damage, liability protection, and loss of rental income. Additionally, landlords can implement proactive maintenance routines to minimize the risk of property damage and ensure tenants’ safety. In a table format, landlords can compare the features of different insurance policies and choose one that best suits their needs: | Insurance Policy | Property Damage Coverage | Liability Protection | Loss of Rental Income | |———————|————————–|———————-|———————–| | Basic Policy | Limited | Basic | No coverage | | Comprehensive Policy| Extensive | Enhanced | Extended coverage | By taking these proactive measures, landlords can effectively manage risks even when landlord insurance expires, safeguarding their investment and ensuring the security of their tenants.Communication With Tenants

Communication with tenants is crucial when it comes to addressing the status of landlord insurance. Informing tenants about the insurance status and addressing their concerns is vital for maintaining a transparent and harmonious landlord-tenant relationship.

Informing Tenants About Insurance Status

Informing tenants about the insurance status should be a priority for landlords. They should clearly communicate the expiration of the landlord insurance policy to tenants well in advance. Issuing a notice or sending an email detailing the expiration date and the steps being taken to renew or update the policy can help keep tenants informed and alleviate any concerns.

Addressing Tenant Concerns

Addressing tenant concerns promptly is essential. Landlords should be open to answering any questions or addressing any apprehensions tenants may have about the expired insurance policy. Providing reassurance and updating tenants about the actions being taken to secure new insurance coverage can help alleviate any anxieties they may have about their living situation.

Seeking Professional Advice

When landlord insurance expires, it’s crucial to seek professional advice to ensure you are adequately protected. Consulting insurance agents or brokers and seeking legal advice can provide valuable insights and guidance in navigating the complexities of landlord insurance.

Consulting Insurance Agents Or Brokers

Consulting insurance agents or brokers can be a wise decision when your landlord insurance is about to expire. These professionals are well-versed in the policies offered by various insurance companies and can help you find the best option to suit your needs.

Insurance agents are knowledgeable about the specific requirements for landlord insurance and can provide you with tailored advice based on your property and circumstances. They can help you understand the coverage options, including property damage, liability protection, and loss of rental income.

Working with an insurance agent or broker also simplifies the process of comparing different insurance quotes. They have access to multiple insurance providers, allowing you to explore a range of options and select the most affordable and comprehensive coverage for your property.

Legal Advice For Landlords

Obtaining legal advice is essential when your landlord insurance is expiring. Legal professionals specializing in landlord-tenant law can provide invaluable insights into the legal aspects of insurance coverage.

A legal advisor can help you understand the terms and conditions of your insurance policy, ensuring you have a clear understanding of the coverage, exclusions, and any limitations. They can also assist in the event of a claim dispute or provide guidance on how to handle tenant-related issues that may impact your coverage.

Furthermore, legal advisors can review and draft lease agreements to ensure that they align with your insurance policy requirements. This proactive approach can help mitigate risks and protect your property investment.

By seeking legal advice, you can have peace of mind knowing that you are adhering to legal obligations and taking the necessary steps to protect your interests as a landlord.

Frequently Asked Questions On When Landlord Insurance Expires

How Long Should You Keep Insurance Policies After They Have Expired?

You should keep insurance policies after they have expired for at least 7 years. Keeping them for longer can help with potential disputes or claims.

What Happens When An Insurance Policy Lapses?

When an insurance policy lapses, coverage ends, leaving the policyholder unprotected from any future claims or benefits.

What Happens If Your Homeowners Insurance Lapses?

If your homeowners insurance lapses, you won’t have coverage for any damages or losses. It’s crucial to maintain active insurance to protect your property from unforeseen events. Keep your policy updated to avoid gaps in coverage and ensure your home and belongings are properly safeguarded.

What Happens If You Stop Paying Home Insurance?

If you stop paying home insurance, your policy will likely be canceled, leaving your home unprotected against damage or loss. It’s essential to maintain insurance coverage to ensure financial security in case of unexpected events.

Conclusion

As your landlord insurance nears expiration, plan ahead for seamless coverage continuation. Stay protected and safeguard your investment by renewing without delays. Be proactive and update your policy to avoid any gaps in protection. Keep your property secure with ongoing coverage to ease your worries.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “How long should you keep insurance policies after they have expired?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “You should keep insurance policies after they have expired for at least 7 years. Keeping them for longer can help with potential disputes or claims.” } } , { “@type”: “Question”, “name”: “What happens when an insurance policy lapses?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “When an insurance policy lapses, coverage ends, leaving the policyholder unprotected from any future claims or benefits.” } } , { “@type”: “Question”, “name”: “What happens if your homeowners insurance lapses?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “If your homeowners insurance lapses, you won’t have coverage for any damages or losses. It’s crucial to maintain active insurance to protect your property from unforeseen events. Keep your policy updated to avoid gaps in coverage and ensure your home and belongings are properly safeguarded.” } } , { “@type”: “Question”, “name”: “What happens if you stop paying home insurance?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “If you stop paying home insurance, your policy will likely be canceled, leaving your home unprotected against damage or loss. It’s essential to maintain insurance coverage to ensure financial security in case of unexpected events.” } } ] }

Leave a comment