Liability insurance occurs when a person or business obtains coverage against claims for injuries or damage caused to another party. This type of insurance provides financial protection and helps cover legal expenses if a claim is made against the policyholder for negligence or harm caused to someone else.

It is a critical form of insurance for individuals and organizations to safeguard against potentially costly liabilities and lawsuits arising from accidental injuries, property damage, or other unfortunate incidents. Understanding the need for liability insurance and obtaining suitable coverage tailored to your specific circumstances can offer peace of mind and financial protection when unforeseen events occur.

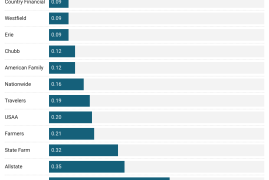

Credit: cavazossentinel.com

Understanding Liability Insurance

What Is Liability Insurance?

Liability insurance is a type of coverage that provides protection for individuals or businesses in case they are held responsible for injury or damage to another person or property.

It essentially helps cover legal costs and payouts for which the insured party would be liable.

Importance Of Liability Insurance

Liability insurance is crucial as it safeguards individuals and businesses from financial ruin in the event of a lawsuit arising from negligence or accidents.

- It offers a sense of security and peace of mind to the insured party.

- Not having liability insurance can expose individuals and businesses to substantial financial risks.

| By having liability insurance, you mitigate the potential for devastating financial losses. |

It is advisable for individuals and businesses to secure liability insurance to protect themselves and their assets.

Credit: http://www.facebook.com

Types Of Liability Insurance

Liability insurance protects individuals and businesses in the event of lawsuits or claims for damages. It provides financial coverage for legal costs and settlements, ensuring that those who are liable for accidents or injuries are held accountable.

Liability insurance is an essential form of protection that shields individuals and businesses from financial loss in case they are found responsible for causing harm to others. There are different types of liability insurance policies designed to cater to specific needs and circumstances. These policies provide coverage for a range of potential liabilities, ensuring that individuals and businesses have the necessary financial protection in place. In this article, we will explore three main types of liability insurance: General liability insurance, Professional liability insurance, and Product liability insurance.

General Liability Insurance

General liability insurance, also known as commercial general liability insurance or CGL, is a policy that provides coverage for third-party bodily injury, property damage, and personal injury claims. This type of insurance is typically purchased by businesses to protect themselves against common liability risks that may arise during their day-to-day operations. General liability insurance offers financial protection in case someone is injured on the premises of a business, or if the business causes damage to someone’s property. It also covers legal expenses if the business is sued for claims of slander, libel, or copyright infringement.

Professional Liability Insurance

Professional liability insurance, often referred to as errors and omissions insurance or E&O insurance, is specifically designed for professionals who provide advice or services to clients. This insurance policy protects professionals from claims arising out of negligence, mistakes, or failure to perform the expected duties in their profession. Professionals such as doctors, lawyers, accountants, consultants, and architects rely on professional liability insurance to safeguard against claims of professional errors or omissions that may lead to financial loss for their clients. This coverage offers peace of mind and financial protection in case a client brings a lawsuit alleging professional negligence or malpractice.

Product Liability Insurance

Product liability insurance is a type of coverage that manufacturers, distributors, and retailers of products can obtain to protect themselves against claims related to the products they sell. This insurance safeguards businesses from financial damages arising from injuries or property damage caused by a product’s defects or flaws. If a defective product causes harm to a consumer and leads to legal action, product liability insurance covers the costs associated with defending against the claim and compensating the injured party. It is an essential form of protection for businesses involved in the manufacturing or sale of products.

Determining Your Coverage Needs

When it comes to determining your liability insurance coverage needs, it’s imperative to begin by assessing your risks. Consider all potential scenarios where your business could be held liable for damages or injuries.

Next, it’s crucial to understand the process of calculating coverage limits. This involves evaluating the worst-case scenarios and estimating the maximum potential costs you may face in the event of a liability claim.

Choosing The Right Insurer

Researching insurance providers is a crucial step when seeking liability coverage. It’s important to evaluate various insurers to find one that best meets your needs and offers competitive terms.

Researching Insurance Providers

Begin by researching and analyzing insurers’ financial strength, customer service reviews, and industry reputation. Look for qualities such as reliability, evidence of satisfied customers, and long-standing presence in the market.

When evaluating potential insurers, consider online reviews, ratings from financial strength agencies, and feedback from business associates to gain a comprehensive understanding of their standing. You can also reach out to industry peers to gather firsthand insights.

Comparing Quotes And Services

Obtaining quotes from multiple insurers is essential to ensure you’re getting the best coverage at a competitive rate. To compare quotes thoroughly, create a summary table of each policy’s coverage limits, deductibles, and premium costs.

Review the scope of coverage provided by each insurer, making sure they align with your business’s unique needs. Don’t forget to inquire about any additional services or customizable policies to accommodate specific requirements.

Factors Affecting Premiums

There are several factors that can affect the premium of your liability insurance. Understanding these factors can help you make informed decisions as you choose the right coverage for your business. The three key factors influencing insurance premiums are:

Business Size And Industry

The size and industry of your business play a significant role in determining your liability insurance premium. Different industries come with varying risks, and insurance providers take this into account when calculating premiums. For example, high-risk industries like construction and healthcare may require higher coverage limits and therefore have higher premiums. Additionally, larger businesses may have higher premiums due to increased exposure and potential for higher claims.

Claims History

The claims history of your business is another crucial factor insurers consider when determining your liability insurance premiums. If your business has a history of frequent claims or high claim amounts, insurance providers may consider your business as high risk and charge a higher premium. Conversely, businesses with a clean claims history may be eligible for lower premiums as they are perceived as a lower risk.

Coverage Limits

The coverage limits you select for your liability insurance can impact the premium you pay. Higher coverage limits mean more comprehensive protection, but they also result in higher premiums. On the other hand, lower coverage limits may reduce your premiums but leave you exposed to potential risks if a larger claim arises. It is important to carefully assess your business needs and find the right balance between adequate coverage and manageable premiums.

Maximizing Your Protection

When it comes to liability insurance, maximizing your protection is crucial. By fully understanding policy exclusions and exploring add-ons for enhanced coverage, you can ensure comprehensive protection for your assets.

Understanding Policy Exclusions

Policy exclusions are conditions under which your liability insurance may not provide coverage.

- Important to grasp to avoid surprises.

- Review your policy carefully.

- Consult with your insurance agent.

Add-ons For Enhanced Coverage

Add-ons can extend the protection offered by your liability insurance policy.

- Consider umbrella insurance for higher coverage limits.

- Special endorsements for industry-specific risks.

- Talk with your insurer about customized options.

Steps To Take In Case Of A Claim

When liability insurance comes into play, it’s crucial to be prepared and know the necessary steps to take in case of a claim.

Contacting Your Insurer

- Immediately notify your insurance company about the incident.

- Provide details regarding the claim and any relevant information.

- Follow any specific instructions given by your insurer regarding the claim process.

Gathering Documentation

- Collect evidence such as photos, videos, and witness statements if possible.

- Keep records of all communications with the insurer and any parties involved.

- Provide necessary documents like police reports, medical bills, and receipts.

Reviewing And Updating Your Policy

When it comes to liability insurance, reviewing and updating your policy is a crucial step to ensure that you have the appropriate coverage for your current situation. By regularly reviewing and updating your policy, you can make sure that you are adequately protected against potential liabilities.

Annual Policy Review

An annual policy review is essential to assess whether your current liability coverage aligns with your current needs and circumstances. Reviewing your policy annually enables you to stay informed about any changes in coverage, limits, or exclusions that may affect your liability protection.

Adjusting Coverage Based On Changes

As your business or personal situation evolves, your liability insurance needs may also change. It’s important to remain vigilant and adjust your coverage accordingly. Review your policy to see if any changes, such as business expansion, new assets, or increased risk exposure, necessitate adjusting your coverage levels to reflect your current situation accurately.

Ensuring Each Heading Adheres To Html Syntax

Make sure that each H3 heading in your policy reflects the most up-to-date information and adequately covers your current liabilities. It’s crucial to maintain a proactive approach in managing your liability insurance to ensure that you are adequately protected against unforeseen risks. Regularly reviewing and updating your policy helps you stay ahead of any potential gaps in coverage and maintain peace of mind.

:max_bytes(150000):strip_icc()/buildawall.asp_Final-a5c4a02c9bf94fef9d648d7439cf0749.png)

Credit: http://www.investopedia.com

Frequently Asked Questions On When Liability Insurance Happen

What Is Liability Insurance And How Does It Work?

Liability insurance provides financial protection for the insured party in case of legal liabilities. It covers legal costs, settlements, and other expenses that may arise from claims against the insured. It’s essential for businesses and individuals to mitigate risks and protect assets.

What Types Of Liabilities Are Covered By Liability Insurance?

Liability insurance typically covers bodily injury, property damage, personal injury, and advertising injury. It can also extend to cover products liability and completed operations liability. Understanding the specific coverage is crucial for businesses and individuals to ensure comprehensive protection against potential risks.

When Does Liability Insurance Come Into Play?

Liability insurance comes into play when an insured party is legally responsible for damages to another party. This may result from accidents, negligence, or other covered events. The insurance provider will handle legal obligations, such as defending against lawsuits and covering settlement payments, up to the policy’s limits.

Conclusion

Considering the unpredictable nature of accidents, liability insurance emerges as a crucial protective measure. With its coverage and financial support, individuals and businesses can navigate legal complexities and potential lawsuits more confidently. By safeguarding against potential losses and legal expenses, liability insurance ensures peace of mind and allows for smooth business operations.

Its benefits, such as protecting assets and reputation, cannot be overstated. So, investing in liability insurance becomes an essential step for all parties involved. Remember, preparedness is always preferable to regret.

Leave a comment