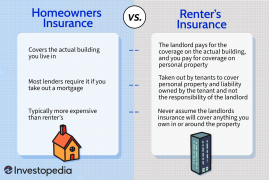

Homeowners insurance is expensive due to increased natural disasters and higher replacement costs of homes. Many factors influence the pricing of homeowners insurance, making it a substantial investment for homeowners.

Factors such as the location of the property, the age and condition of the home, the coverage limits, and the homeowner’s claims history all play a role in determining the cost of the policy. Additionally, insurance companies consider the risk associated with insuring a particular property, such as the likelihood of weather-related damages or burglary.

As a result, homeowners may find themselves paying higher premiums to adequately protect their investment in their property. It is essential for homeowners to understand these factors and shop around to find the best coverage at a reasonable price.

1. Factors Affecting Homeowners Insurance Costs

1.1 Location

The geographical location of your home plays a crucial role in determining homeowners insurance costs.

1.2 Age And Condition Of Home

Older homes or those in poor condition may have higher insurance premiums due to increased risks.

1.3 Value Of Property

The higher the value of your property, the more expensive your insurance premium is likely to be.

1.4 Coverage Amount

The more coverage you need, the higher your insurance costs, as it increases the insurer’s potential liability.

1.5 Type Of Policy

The type of policy you choose, such as basic or comprehensive coverage, will significantly impact your insurance rates.

2. Natural Disasters And Homeowners Insurance

2. Natural Disasters and Homeowners Insurance

2.1 Impact Of Natural Disasters On Premiums

Natural disasters such as hurricanes, earthquakes, and wildfires can significantly impact homeowners insurance premiums.

2.2 High-risk Areas And Costs

Living in high-risk areas prone to natural disasters may result in higher homeowners insurance costs.

2.3 Mitigating Natural Disaster Costs

Mitigating natural disaster costs can be done through proper home maintenance, upgrading to resilient materials, and installing safeguards like home security systems.

3. Personal Factors And Homeowners Insurance

When it comes to determining the cost of homeowners insurance, various personal factors come into play. Insurers consider these factors to assess the level of risk associated with providing coverage. Understanding how these personal factors affect your premiums can help you make informed decisions about your home insurance policy. Let’s explore some important personal factors and their impact on insurance costs:

3.1 Credit Score And Insurance Costs

A person’s credit score plays a significant role in determining their homeowners insurance rates. Insurers have found that individuals with lower credit scores tend to file more claims, leading to higher insurance costs. This is why they consider your credit score when calculating your premiums.

Your credit score reflects your financial responsibility and helps insurers assess the likelihood of you making a claim. So, it’s important to maintain a good credit score to enjoy more affordable homeowners insurance rates. Improving your credit score can provide significant savings in the long run.

3.2 Claims History And Premiums

Your claims history is another personal factor that can impact your homeowners insurance premiums. Insurers review your past claims and take them into consideration when determining your rates. If you have a history of multiple claims or high-value claims, insurers may consider you a higher risk, resulting in higher premiums.

On the other hand, homeowners with few or no recent claims might be eligible for discounted premiums. By maintaining a claim-free history, you demonstrate to insurers that you are a responsible homeowner with lower risk. This can lead to potential cost savings on your insurance policy.

3.3 Home Security And Insurance Savings

Investing in home security measures not only provides peace of mind but can also lead to significant insurance savings. Insurers often offer discounts for homeowners who have installed security systems, smoke detectors, and burglar alarms. These devices reduce the risk of theft, fire, and other damages, making your home safer and less likely to require a claim.

By enhancing your home’s security, you demonstrate to insurers that you are taking proactive steps to protect your property, resulting in potential premium savings. Remember to document your security upgrades and inform your insurance provider to ensure you receive any applicable discounts.

4. Role Of Insurance Providers

When it comes to the cost of homeowners insurance, the role of insurance providers is a crucial factor. There are several aspects within the insurance industry that contribute to the high costs of homeowners insurance, including underwriting and risk assessment, profit margins and business expenses, as well as competition and market dynamics.

4.1 Underwriting And Risk Assessment

Underwriting and risk assessment play a significant role in determining the cost of homeowners insurance. Insurance providers assess the risk associated with insuring a particular property, considering factors such as the location, construction type, age of the property, and previous insurance claims. This process helps insurers evaluate the likelihood of potential losses, which directly impacts the premium rates charged to homeowners.

4.2 Profit Margins And Business Expenses

Profit margins and business expenses also contribute to the high cost of homeowners insurance. Insurance providers aim to generate profits while covering their operational costs, claims payouts, and reinsurance expenses. As a result, the premiums charged by insurers include a margin for profitability and provisions for anticipated expenses, which can drive up the overall cost of insurance for homeowners.

4.3 Competition And Market Dynamics

Competition and market dynamics exert influence on the pricing of homeowners insurance. In a competitive insurance market, insurers may adjust their premium rates in response to industry trends, regulatory changes, and shifts in consumer demand. Additionally, market dynamics, such as catastrophic events and natural disasters, can impact insurers’ risk exposure and pricing strategies, ultimately affecting the affordability of homeowners insurance.

5. Available Discounts And Savings

5. Available Discounts and Savings

5.1 Bundle Policies For Savings

Combining your homeowners insurance with your auto insurance can often lead to a significant discount. Insurance companies often offer discounts when you purchase multiple policies from them, so make sure to inquire about potential savings by bundling your insurance policies together.

5.2 Installing Security Systems

Installing a security system in your home can not only provide peace of mind but also potentially lead to discounts on your homeowners insurance. Many insurance companies offer discounts for homes with security systems, as they are seen as a lower risk for potential theft or damage.

5.3 Age Of Home And Discounts

The age of your home can also impact your insurance premiums. Some insurance providers offer discounts for newer homes, as they are less likely to have certain structural issues or damage. Be sure to inquire about potential discounts based on the age of your home when shopping for homeowners insurance.

5.4 Maintaining A Good Credit Score

Insurance companies often take your credit score into account when determining your homeowners insurance premiums. Maintaining a good credit score can result in lower insurance rates. Be sure to stay on top of your credit score and work towards improving it, as it can directly impact the cost of your homeowners insurance.

6. The Importance Of Shopping Around

Homeowners insurance can be pricey, so shopping around is crucial. It’s important to compare quotes from various providers to find the best coverage at the most competitive price. By taking the time to shop around, homeowners can potentially save money while ensuring they have adequate protection for their homes.

6.1 Comparing Quotes From Different Providers

When it comes to homeowners insurance, it’s essential to shop around and compare quotes from different providers. This simple step can help you find the best coverage at the most affordable price. Each insurance company has its own way of assessing risk factors, which means that the premiums they offer can vary significantly.

By comparing quotes, you can ensure that you are getting the best value for your money. You can easily do this by visiting the websites of various insurance providers and requesting quotes. Make sure to provide accurate information about your property to get the most accurate quotes.

Keep in mind that choosing the cheapest option isn’t always the best decision. It’s important to consider the coverage limits, deductibles, and any additional features before making a final decision. A slightly higher premium might be worth it if it provides more comprehensive coverage and better customer service.

6.2 Considering Customer Reviews And Ratings

Customer reviews and ratings can provide valuable insights into the quality of service and claims handling of different homeowners insurance providers. Considering these reviews can give you a better idea of what to expect if you need to file a claim in the future.

Look for reputable websites that aggregate customer reviews, such as Consumer Reports or the Better Business Bureau. Pay attention to feedback regarding the claims process, timely responses, and overall customer satisfaction. A provider with positive reviews and high ratings is more likely to provide a smoother, stress-free experience when you need it most.

6.3 Utilizing Independent Insurance Agents

Another effective way to find the right homeowners insurance policy is to utilize independent insurance agents. These professionals work with multiple insurance companies and can provide you with quotes and policies from various providers. By working with an independent agent, you can save time and effort, as they can do the research and comparison-shopping for you.

An independent agent can also provide you with valuable advice and guidance, helping you understand the details of different policies and determining the best coverage for your specific needs. Their expertise can be particularly helpful if you have unique circumstances, such as owning a historic home or living in an area prone to natural disasters.

7. Balancing Coverage And Affordability

7. Balancing Coverage and Affordability

7.1 Assessing Risk Tolerance

Understanding your risk preference helps determine the right level of homeowners insurance coverage.

7.2 Adjusting Deductibles And Premiums

Higher deductibles can lower premiums but may lead to more out-of-pocket costs in case of a claim.

7.3 Evaluating Additional Coverage Options

Consider additional coverage like flood or earthquake insurance based on your specific needs.

8. Understanding Policy Exclusions

Homeowners insurance can be expensive due to various factors, one of which is policy exclusions. It’s crucial to understand what is not covered under your policy.

8.1 Common Exclusions In Homeowners Insurance

Common exclusions in homeowners insurance policies include earthquakes, floods, pest infestations, and wear and tear. These are typically not covered in standard policies.

8.2 Optional Add-ons For Coverage

Optional add-ons, also known as endorsements, can provide additional coverage for excluded items. Examples include flood insurance, earthquake coverage, and personal property endorsements.

Frequently Asked Questions On Why Is Homeowners Insurance So Expensive

Why Do Homeowners Insurance Rates Keep Going Up?

Homeowners insurance rates may increase due to various factors such as a rise in construction costs, inflation, natural disasters, and increased claims. Insurance companies adjust their pricing to manage risk and maintain financial stability.

What Factors Impact The Cost Of Homeowners Insurance?

Several factors impact the cost of homeowners insurance, including the property’s location, age, type of construction, coverage limits, deductible amount, and the homeowner’s credit score. Additionally, the presence of security systems, fire alarms, and smoke detectors may also influence pricing.

How Can Homeowners Lower Their Insurance Premiums?

Homeowners can lower their insurance premiums by bundling policies, maintaining a good credit score, enhancing home security, and undertaking preventive maintenance. Additionally, it’s beneficial to compare quotes from multiple insurance providers and consider adjusting coverage levels based on individual needs.

Conclusion

Homeowners insurance can be expensive due to a variety of factors. Factors such as location, construction materials, and the value of your property can impact the cost. Additionally, risks such as natural disasters, theft, and liability claims can also contribute to higher premiums.

It is crucial to carefully review and compare insurance policies to find the best coverage at an affordable price. By understanding the factors that drive the cost of homeowners insurance, you can make informed decisions and potentially lower your insurance expenses.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “Why do homeowners insurance rates keep going up?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Homeowners insurance rates may increase due to various factors such as a rise in construction costs, inflation, natural disasters, and increased claims. Insurance companies adjust their pricing to manage risk and maintain financial stability.” } } , { “@type”: “Question”, “name”: “What factors impact the cost of homeowners insurance?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Several factors impact the cost of homeowners insurance, including the property’s location, age, type of construction, coverage limits, deductible amount, and the homeowner’s credit score. Additionally, the presence of security systems, fire alarms, and smoke detectors may also influence pricing.” } } , { “@type”: “Question”, “name”: “How can homeowners lower their insurance premiums?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Homeowners can lower their insurance premiums by bundling policies, maintaining a good credit score, enhancing home security, and undertaking preventive maintenance. Additionally, it’s beneficial to compare quotes from multiple insurance providers and consider adjusting coverage levels based on individual needs.” } } ] }

Leave a comment