Liability with insurance refers to the legal responsibility a person or entity has for damages or losses covered by an insurance policy. Insurance coverage provides financial protection for individuals and businesses in case they are found responsible for causing bodily injury or property damage to others.

These policies typically cover the costs of legal defense and any settlements or judgments that arise from the covered claim. Liability insurance is essential for protecting individuals and businesses from the financial burdens that can result from lawsuits or accidents.

Whether it’s a car accident, a slip and fall on your property, or a professional mistake, liability insurance ensures that you are not personally responsible for the expenses. By understanding how liability insurance works, individuals and businesses can better manage their risks and protect their financial interests. We will explore the concept of liability insurance in detail and discuss its various types and benefits.

Credit: fastercapital.com

Types Of Liability Insurance

Understanding the various types of liability insurance is crucial for protecting businesses from potential financial losses. Here are the main categories:

General Liability Insurance

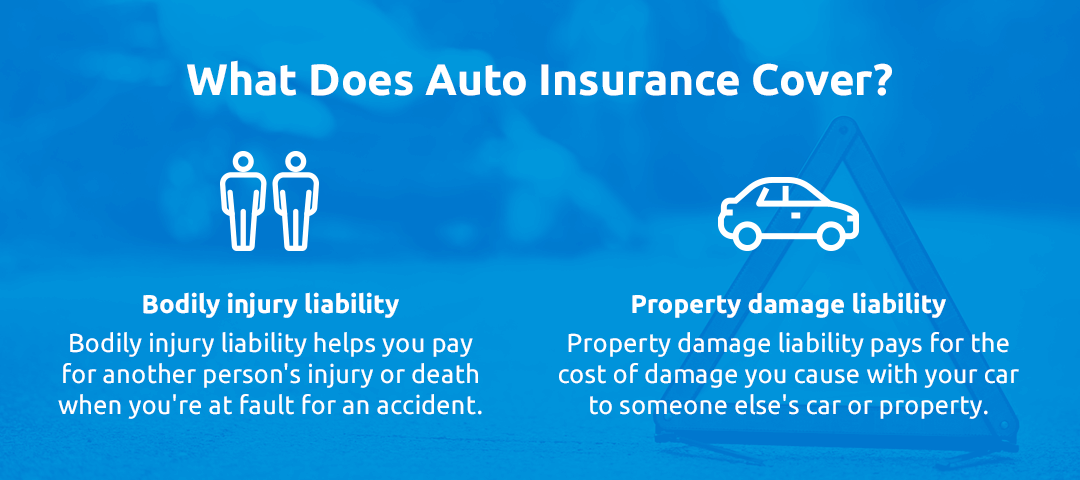

General Liability Insurance covers third-party claims of bodily injury, property damage, and advertising injury.

Professional Liability Insurance

Professional Liability Insurance protects professionals against negligence claims stemming from professional services.

Product Liability Insurance

Product Liability Insurance shields businesses from financial losses due to defective products causing harm.

Coverage Limits And Exclusions

In insurance, liability coverage limits and exclusions play a crucial role in determining the extent of protection provided by your policy. Understanding these aspects is essential to ensure you have the right coverage for your needs. Let’s delve into coverage limits and common exclusions in liability insurance:

Understanding Coverage Limits:

Liability insurance policies have coverage limits that determine the maximum amount your insurer will pay for a covered claim. These limits are typically defined as a split limit or a combined single limit (CSL).

Split Limit:In a split limit policy, your coverage limits are divided into different amounts for bodily injury per person, bodily injury per accident, and property damage per accident. For example, a policy may have limits of $50,000 per person, $100,000 per accident for bodily injury, and a limit of $50,000 for property damage.

Combined Single Limit (CSL):A combined single limit policy does not distinguish between bodily injury and property damage. Instead, it provides a single total limit that applies to all covered claims resulting from an accident. For instance, a CSL policy with a limit of $300,000 means that this amount is available to cover both bodily injury and property damage claims.

When selecting your coverage limits, it’s essential to consider the potential costs associated with injuries or damage that may result from an accident. Higher coverage limits provide greater financial protection, but they also come with higher premiums.

Common Exclusions In Liability Insurance:

While liability insurance provides valuable protection, it’s important to be aware of the common exclusions found in policies. Exclusions are situations or events that the insurance company will not cover.

Intentional Acts:Liability insurance does not cover intentional acts, such as intentionally causing harm or damage to others. It is designed to protect against accidental or negligent actions only.

Professional Liabilities:Most liability insurance policies exclude coverage for professional liabilities. If you work in a profession where you provide advice or services, such as a doctor or lawyer, you may need a separate professional liability insurance policy to protect against claims related to your profession.

Automobile-related Exclusions:Liability insurance for personal vehicles usually excludes coverage for accidents that occur while using your vehicle for business purposes. Additionally, actions like racing or using your vehicle for illegal activities may also be excluded.

Hazardous Activities:Engaging in certain hazardous activities, such as skydiving or rock climbing, may be excluded from general liability coverage. If you participate in these activities, you may need to obtain specific coverage tailored to these risks.

Employee Injuries:Liability insurance typically does not provide coverage for injuries to your employees. Workers’ compensation insurance is typically required to address workplace injuries.

War and Terrorism:Damage or liability resulting from acts of war or terrorism are commonly excluded from liability insurance policies.

Understanding coverage limits and exclusions is vital to ensure you have the right liability insurance policy for your needs. Be sure to carefully review your policy and consult with your insurance provider to fully understand the specifics of your coverage.

Determining Your Liability Coverage Needs

When it comes to liability coverage with insurance, determining your needs is vital to ensuring adequate protection against potential risks. Liability coverage safeguards individuals and businesses from legal claims and financial losses in case of bodily injury, property damage, or other liabilities. As each situation is unique, determining the right amount of liability coverage requires a methodical approach.

Assessing Risks

Start by evaluating the potential risks associated with your personal or business activities. Identify vulnerable areas where accidents or mishaps could occur, and consider the possible financial implications. This assessment helps in determining the level of liability coverage needed to protect against potential lawsuits and settlements.

Consulting With Insurance Agent Or Broker

Engage with a qualified insurance agent or broker who can provide expert insights and guidance regarding liability coverage. Discuss your individual circumstances and risks, and seek their expertise in determining the appropriate coverage amount. An experienced professional can offer tailored recommendations to ensure comprehensive protection.

Key Factors Impacting Liability Insurance Premiums

When it comes to liability insurance, several key factors can impact the premiums businesses pay. Understanding these factors is essential for devising a tailored insurance strategy that meets specific business needs while managing costs effectively. Here, we delve into the critical elements that influence liability insurance premiums.

Business Size And Operations

The size and operations of a business are crucial determinants of liability insurance premiums. Large businesses with extensive operations and numerous employees may face higher premiums due to the potentially greater exposure to risks, while small businesses typically attract comparatively lower premiums. Moreover, companies in high-risk industries or those that engage in hazardous activities can expect higher premiums due to the elevated likelihood of claims.

Claims History

An organization’s claims history directly affects its liability insurance premiums. Businesses with a track record of frequent claims or significant settlements may encounter increased premiums as insurers view them as higher-risk clients. Conversely, companies with a clean claims history are perceived as lower-risk clients, likely qualifying for more favorable premium rates. Maintaining a proactive approach to risk management and safety measures can help mitigate future claims and consequently influence premium rates positively.

Industry

The industry in which a business operates is a fundamental consideration in determining liability insurance premiums. Certain sectors, such as construction, healthcare, and manufacturing, inherently involve higher levels of risk, which can translate into elevated insurance costs. Conversely, industries with lower risk profiles, such as professional services or technology, may benefit from more competitive premium rates. Understanding the risk profiles associated with specific industries is essential for businesses to accurately anticipate insurance expenses and adopt appropriate risk mitigation strategies.

Legal Implications Of Inadequate Liability Coverage

Understanding liability coverage is crucial for anyone looking to protect themselves or their business from potential legal and financial repercussions. Without adequate liability coverage, individuals and businesses may find themselves exposed to lawsuits and significant financial losses. Moreover, failing to comply with legal requirements can have serious consequences. In this article, we explore the legal implications of inadequate liability coverage under two main subheadings: lawsuits and financial losses and compliance with legal requirements.

Lawsuits And Financial Losses

Inadequate liability coverage can leave individuals and businesses vulnerable to lawsuits and substantial financial losses. When a legal claim is filed against someone who lacks sufficient coverage, they may be responsible for paying all damages and legal fees out of their own pocket. This can result in a significant drain on personal and business finances, potentially leading to bankruptcy or the closure of a business.

Without adequate coverage, individuals and businesses may also face the possibility of losing their assets, such as homes, vehicles, or savings, to satisfy judgments or settlements. Additionally, lacking proper liability coverage can damage a person’s or business’s reputation, affecting their ability to secure future contracts or business opportunities.

Consider the scenario of a small business owner who operates a bakery. If a customer were to suffer an injury due to a slip and fall accident on the bakery’s premises, inadequate liability coverage could lead to a lawsuit. Without sufficient coverage, the business owner may be required to pay medical expenses, lost wages, and legal fees, potentially leading to severe financial strain or even closing the bakery altogether.

Compliance With Legal Requirements

Inadequate liability coverage can also result in non-compliance with legal requirements. Depending on the jurisdiction and the industry, there are often specific liability insurance mandates that businesses and individuals must adhere to. These requirements vary widely, ranging from minimum coverage limits to mandatory coverage for certain types of businesses.

Failing to comply with these legal requirements can result in penalties, fines, or even legal consequences. Insurance regulators and government agencies are responsible for ensuring compliance and may impose sanctions or penalties on those found to be operating without adequate liability coverage. Non-compliance can not only put a person’s or business’s financial stability at risk but also damage their reputation and standing within their industry.

Summary:

Legal implications of inadequate liability coverage include exposure to lawsuits, potential asset loss, financial strain, and non-compliance with legal requirements. It is essential for individuals and businesses to carefully assess their liability coverage needs and ensure they have proper protection to mitigate these risks.

Credit: http://www.insurancecentermo.com

Tips For Maximizing And Optimizing Your Liability Coverage

Unveiling tips for enhancing liability coverage to shield against unforeseen incidents. Ensure maximum protection by optimizing insurance liability effectively.

Reviewing And Updating Policies Regularly

Regular review and updates of insurance policies are essential to ensure adequate coverage.

Bundling Policies For Cost Savings

Opt for bundling different insurance policies to maximize savings without compromising coverage.

Credit: murraylawgroup.com

Frequently Asked Questions For What Is Liability With Insurance

What Is Liability Insurance?

Liability insurance provides financial protection for a person or business in the event of a claim or lawsuit. It covers costs associated with legal defense and any resulting payouts if the insured party is found legally responsible.

What Does Liability Insurance Cover?

Liability insurance covers bodily injury, property damage, and legal costs related to covered claims. It also provides coverage for medical expenses, legal defense fees, and settlements or judgments that the insured party is found liable to pay.

Why Is Liability Insurance Important?

Liability insurance is important as it helps protect individuals and businesses from financial loss due to lawsuits. It provides peace of mind and protects assets by covering legal costs and payouts, ensuring that the insured party is not personally liable for claims made against them.

Conclusion

Understanding liability with insurance is crucial for protecting yourself financially. Without liability coverage, you could be held responsible for paying the costs of accidents or injuries. By having the right insurance policy, you can breathe easy knowing that you are financially protected.

It’s important to review your policy regularly to ensure you have the right amount of coverage for your needs. Don’t wait until it’s too late – take action now to ensure your liability coverage is in place.

Leave a comment